2026 CAGNY Preview: 3 Things We Think, 3 “Must Sees” (UL, PEP, IFF, UTZ) & What’s Overblown

3 things we think:

Upstarts are gaining in most food & beverage categories, and that’s a structural headwind for the leaders. Superior co-manufacturing availability, more data driven retailer procurement and lower barriers to entry in marketing (e.g. influencers, social media) have enabled increased success for upstart brands (e.g. Goodles, Millie Moon).

CPG companies with pricing power are going to have sustained upward revisions because costs are falling. The sector weighted Optimal Cost Factor remains down sharply (-10.7%) y/y giving a measurable H1 EPS tailwind to otherwise challenged CPG companies (HSY, MDLZ most) relative to planning period (early fall) expectations.

Alignment issues inside CPG companies prevent them from going where the data leads. While CPG companies enjoy vastly greater capabilities to understand their end customer, we think their front line leaders still regard retailers’ interests as primary. This was made crystal clear in the aftermath of COVID when manufacturer gross margins fell despite insufficient capacity. It remains true today, but the implications vary widely by category. We think companies in high velocity categories (e.g. beverages, snacks) & single serve consumables (e.g. candy) have the best ability to cash in on consumer insights. For others, we suggest focus on what is true versus what should be true.

3 must sees:

Figure 1: CAGNY Schedule

| Tuesday | Wednesday | Thursday | Friday | |

| 17-Feb | 18-Feb | 19-Feb | 20-Feb | |

| 7:00 | KHC | |||

| 8:00 | GIS | CHD | Kerry | CL |

| 9:00 | CAG | PEP | PG | L’Oreal |

| 10:00 | KO | PM | RB | COCO |

| 11:00 | JBS | BTI | KMB | NWL |

| 1:00 | ULVR | MO | IFF | |

| 2:00 | MDLZ | SJM | CLX | |

| 3:00 | SYY | UTZ | USFD | |

| 4:00 | INGR | HRL | ELF | |

| 5:00 | MKC | TAP | CELH |

Unilever. Fresh from a successful spinoff of Magnum Ice Cream Company (which we think remains undervalued), we think Unilever still has massive (300 bps+) margin opportunty relative to peers. It also has more potential to reshape its broad portfolio. With an enviable context of superior category/country combinations – selling high gross margin items in geographies with population growth — it has as good a chance of any company of unveiling incremental positive news this week.

Pepsico. Fresh off a courageous & effective pricing reset including an impressive double digit gain in distribution, we expect more substantive supporting data points — particularly in Q&A. If there aren’t more data points, we expect a lot more questions.

IFF. With a strong management team represented by a seasoned & popular CFO Michael DeVeau, a reasonable valuation, lots of non-dollar revenue and a labyrinthine business model that is very sticky but poorly understood, we’re very confident in some positive takeaways. There is no company in staples more capable of profitable self-help regardless of the macro environment.

Honorable mention: Utz. PEP’s planned share gain has to come from somewhere. Among presenters, UTZ will have the most relevant perspective, and the most risk.

3 themes that are likely overblown:

AI as threat/opportunity. At this juncture, AI is changing the world but seems neither an accelerant nor much of an incremental disruptor to most CPG companies. For example, it can make the tools of customer acquisition less expensive – both in terms of using big data & creating content – but it’s unclear to whom those savings accrue. This is a complicated balance sheet of impacts, but the loss of share by big brands over the past 10 years of AI deployment would suggest it’s not likely to be leading brands.

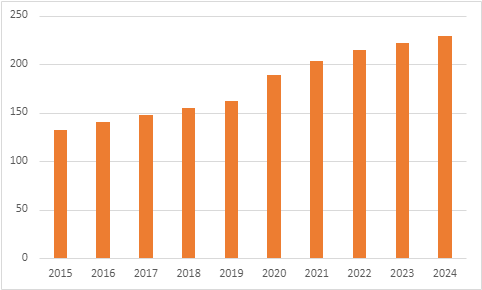

U.S. alcohol consumption is in structural decline based on consumer choice. Recently, the hangover from an alcohol supply glut driven by low interest rates, a demand shock from work-from-home and expanded expectations has driven an emerging consensus that U.S. consumer spending on alcohol is in secular decline. This is bolstered by widespread surveys noting disturbing declines in self-reported alcohol consumption amidst alternatives like cannabis beverages. While the data is not finalfor 2025, we note that personal consumption expenditure data for alcoholic beverages purchased for off-premises consumption has grown sharply since 2019 – albeit at a slowing rate after the COVID bump. Moreover, we think U.S. away from home alcohol consumption has been challenged by the same factors challenging all consumption away from home (e.g. inflation, GLP-1, immigration policy).

Figure 2: US Personal Consumption Expenditures: Off Premise Alcohol ($bn)

Source: U.S. Bureau of Economic Analysis via FRED

Exploring strategic options. They’ve been thoroughly explored. We think historic shorthand for CPG “go private” valuations (e.g. 8.0x EV/EBITDA) were predicated on different capital market landscapes & more certain growth assumptions. For example, from 1980 -2020, there were far fewer asset classes widely believed to generate 6%-8% low beta returns (not necessarily reality). There was also little reason to believe that center store, high ROIC, food company organic volume growth in that reference period could be anything less than population growth, or that sales could be anything less than U.S. GDP. It’s been a while now – those aren’t the assumptions. While some got deals done (e.g. Kellogg), we see KHC and several other companies’ recent exploration of strategic options as a potential dead end for investors.