That 70’s Show … Current Energy Prices Imply Incoming 4-8% PPI + Sentiment Below 70’s Stagflation-Driven Lows + Housing Freeze-Out; Transactions Slowing, Ticket Up; Optimal Luxury Summit: Macro Monday

In charts below: (1) fuel price correlation to PPI is notable and implies 4-8% PPI inbound; (2) Consumer Sentiment is now below 1970’s stagflation impacts – we unpack income strata; (3) housing activity is in a freeze-out (staying on theme … Bruce Springsteen’s “10th Avenue Freeze Out” was released in 1975); (4) we are seeing transaction count slow – more than offset by ticket price; (5) we will have themes and discussions from our NYC Luxury Summit later this week.

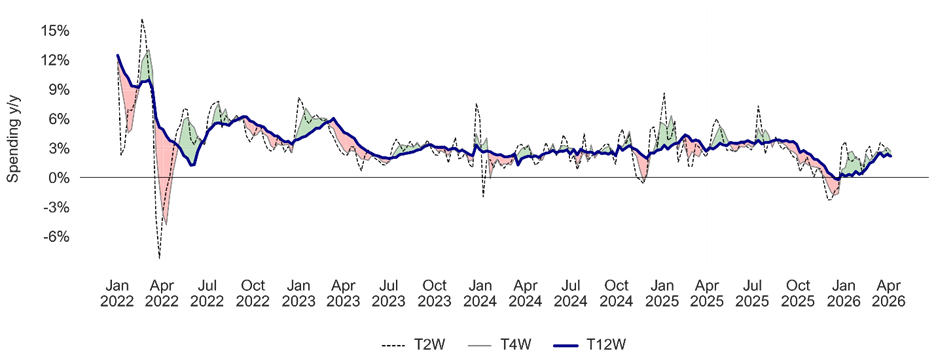

Nominal consumer spending growth decelerated slightly last week by our math – even as gas station spending is now a substantial portion of spending growth. We are seeing more and more signs of spending growth within an across categories made up of less traffic and transactions, offset by higher ticket prices – in our view, this will create demand destruction if conditions persist, and appears to be already doing so in some categories.

As we have discussed, both magnitude and duration of impacts to the consumer always matter – and the combination of higher fuel costs and related higher interest rates are driving (1) lower Sentiment, impacting discretionary spending and (2) we note substantial freeze up of the critical housing transaction cycle (a key precursor to durable good purchases). Lots of 1970’s themes, also echoing that decade … the Orioles are tied for first.

Optimal’s Spring 2026 Luxury Summit with 12 companies across the space is in NYC is Tuesday 4/14 evening. Click Here to Register

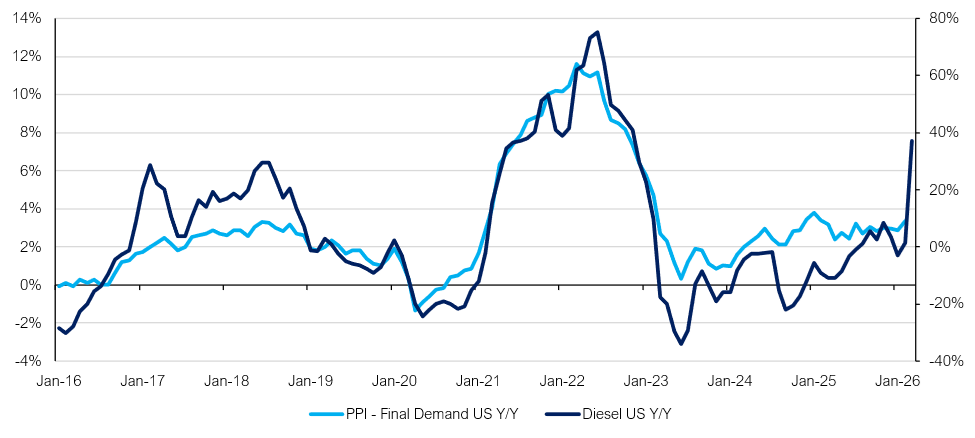

Energy Prices Have Historically Been Very Tied to PPI

Source: Optimal Advisory Analysis, U.S. Energy Information Administration, U.S. BLS, Federal Reserve Bank of St. Louis

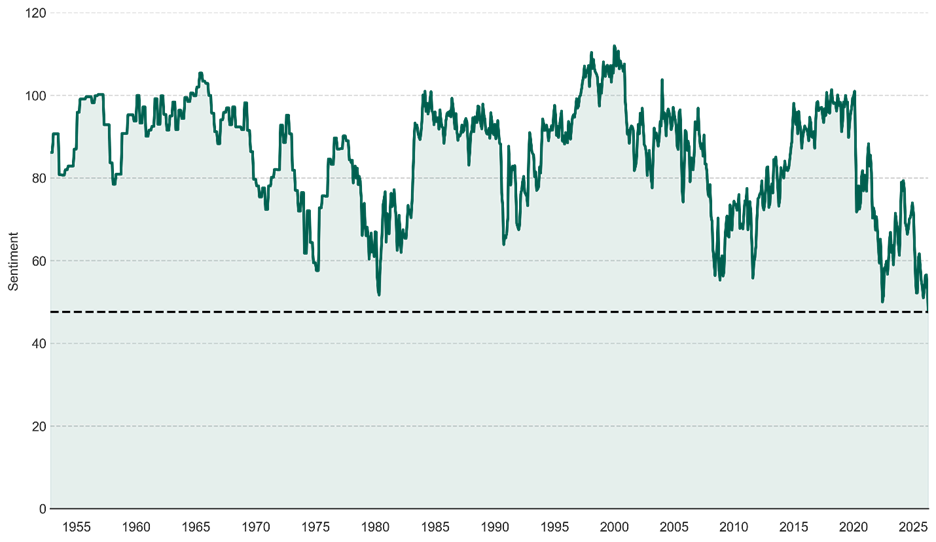

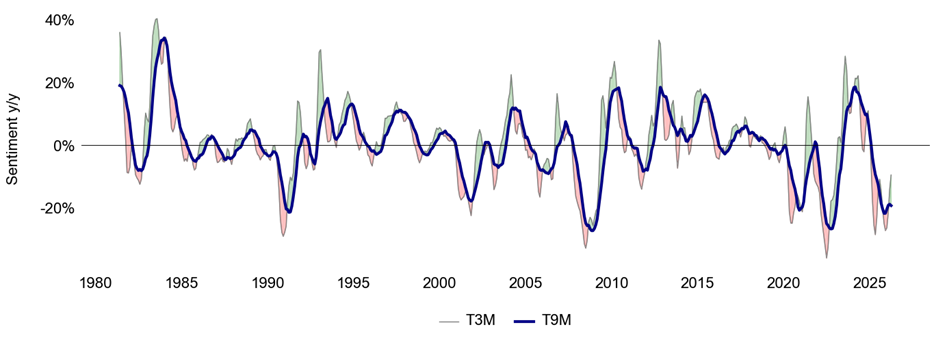

Overall Consumer Sentiment is at All-Time Lows

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey, Federal Reserve Bank of St. Louis

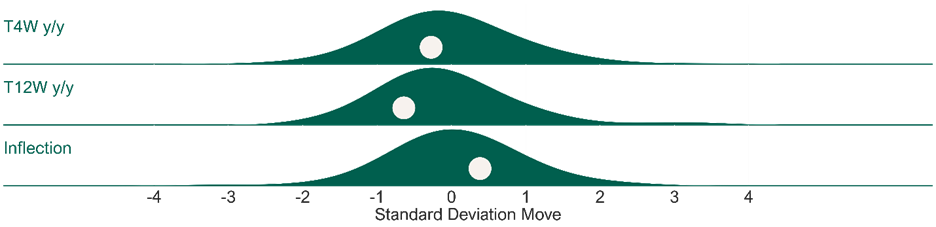

Our Consumer Velocity tracker remained positive but slightly decel’d, up +2.7% y/y T4W following +3.1% y/y last week. This metric was running -1.6% y/y in mid-December but was up +3-4% in 3Q25. The trailing Consumer Velo 12-week trend is up +2.2% y/y (0.6 standard deviations below average) vs. +2.3% y/y the prior week, leading to a +0.5% shorter vs. longer-term inflection (0.4 standard deviations above average). See Fig 1-2.

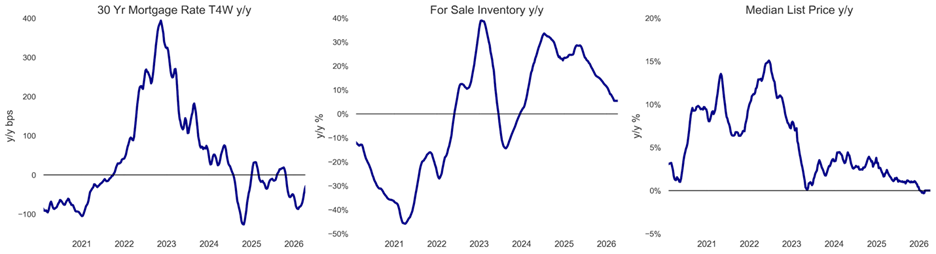

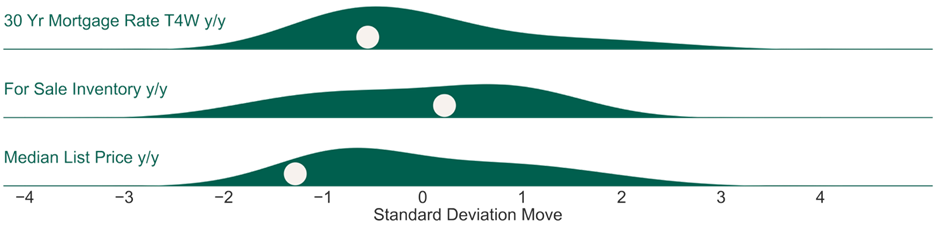

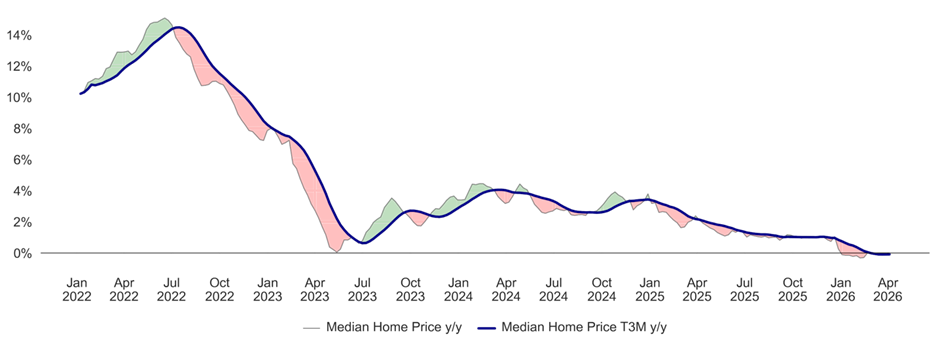

Housing potential & kinetic energy is significantly softer as mortgage rates / bond markets have been pressured higher by oil inflation. US 30Y FRM rate have moved higher in recent weeks, now running down only -29 bps y/y on a T4W basis (0.6 standard deviations below average since 2020). MBA’s mortgage applications for purchase running down -7% y/y while refinance applications running down -4% (refinance applications was running up +100% y/y just 5 weeks ago). Median home prices are flat y/y (1.3 standard deviations below average since 2020). Roughly 18% of Americans sell, build, fix, lend to, and furnish homes – velocity matters for the economy. See Fig 3-6.

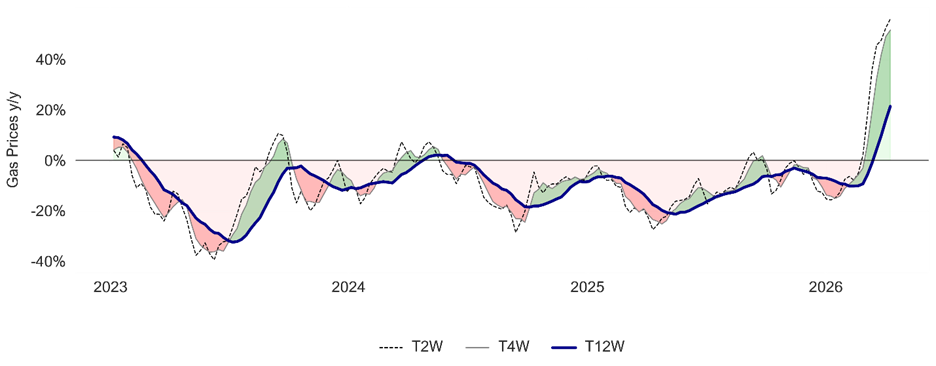

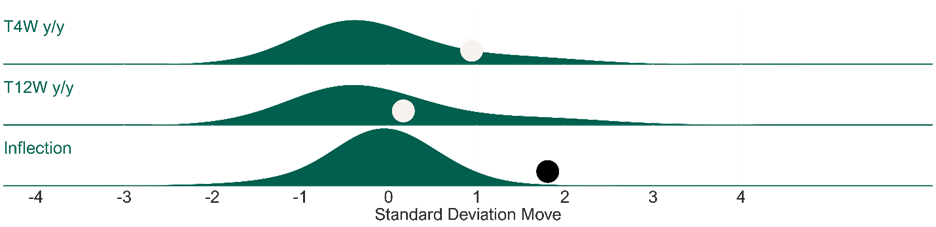

Gasoline inflation is now +51.9% y/y for the week ending last Friday following +60.0% the week prior and +45.4% two weeks ago after gas prices turned down to end the week, although gas prices have since increased again. Gas prices ran up +51.6% y/y on a T4W basis and +21.4% y/y on a T12W basis. It is worth noting US discretionary consumer comp store sales broadly decelerated only after gas y/y prices were +30% in the fall of 2007 (though we do note that $104 WTI crude today is not the same real dollar impact as $114 in 2022 or $140 in 2008). But at the end of the day our analysis of, and experience with, prior slowdowns driven by external macro stimuli suggests gas price inflation of 30%+ y/y begins to impact discretionary spending after about 6-8 weeks. Duration and magnitude of impacts matter. Gas stations started to see a spike in spending around March 7th. Generally, lower-income consumers spend about 5% of their total spend on fuel, and higher-income consumers spend about 2.5% – so a 10% move in gas prices drives 25-50 bp headwind or tailwind. Utilities (electricity and heating fuel) run from about 9% of lower-income household spending to 4% for higher-income households. Duration of change matters – eventually causing Consumer Sentiment shifts, which then drive more or less discretionary spending. See Fig 7-8.

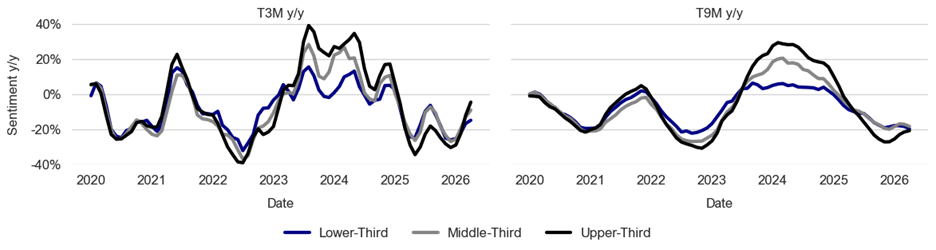

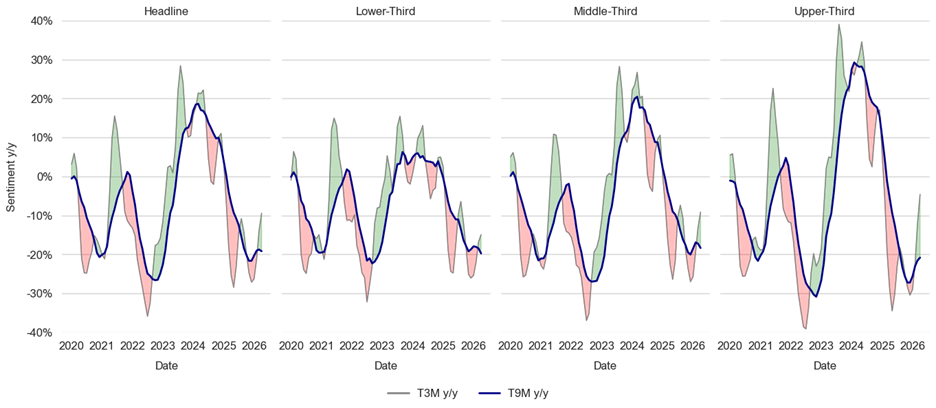

Sentiment is at all-time lows (at 47.6 right now), down -9% y/y this month despite lapping exceedingly weak comparisons. Overall, headline Sentiment is down -9% y/y both this month alone and on a T3M basis (0.8 standard deviations below average) and -19% y/y on a T9M basis (1.8 standard deviations below average). Upper-third income Sentiment has declined -5% y/y on a T3M basis (0.4 standard deviations below average), after declining -12% y/y T3M last month. Middle-income Sentiment has declined -9% y/y on a T3M basis (0.7 standard deviations below average) compared to -13% last month, and lower-income Sentiment has declined -15% y/y on a T3M basis (1.3 standard deviations below average) compared to -17% last month. See Fig 9-12.

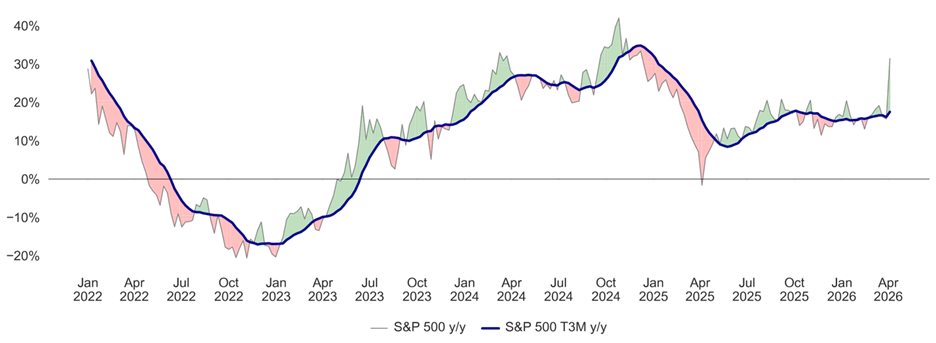

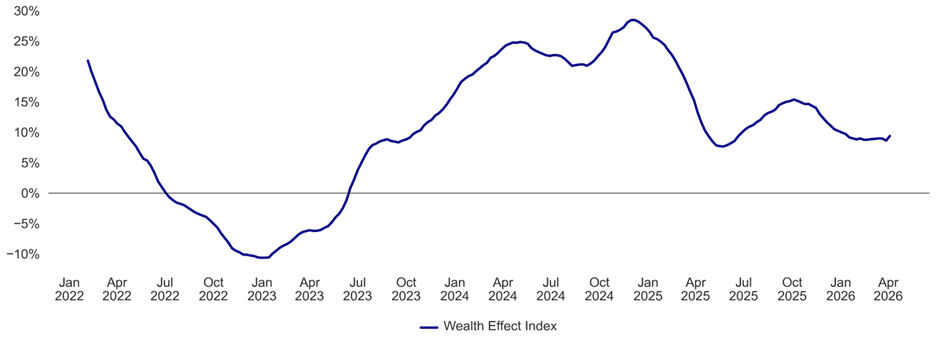

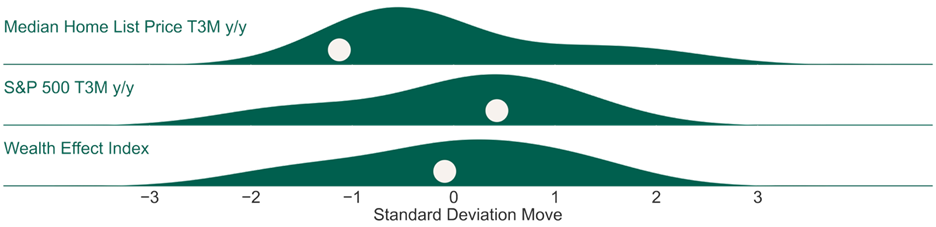

Consumer Wealth Effect Index is nearly 600 bp below 3Q25 levels – a drag on Premium mindset. Optimal Advisory’s Wealth Effect Index is at +9.4% y/y (0.1 standard deviations below average since the start of 2022). This metric was running +15.4% y/y in October 2025. Equity returns are beginning to lap a softer market from April 2025, but with home prices flat y/y and equity returns more volatile in recent weeks we note the “flywheel” of wealth effect is more muted. See Fig 13-16.

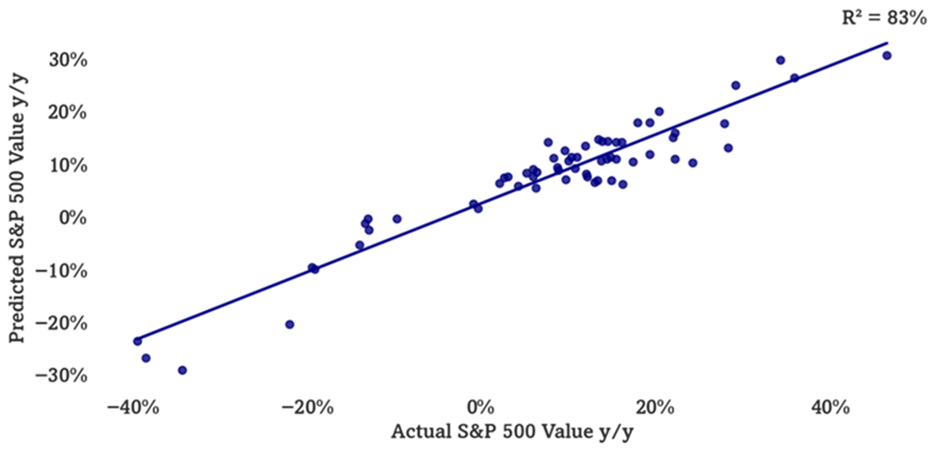

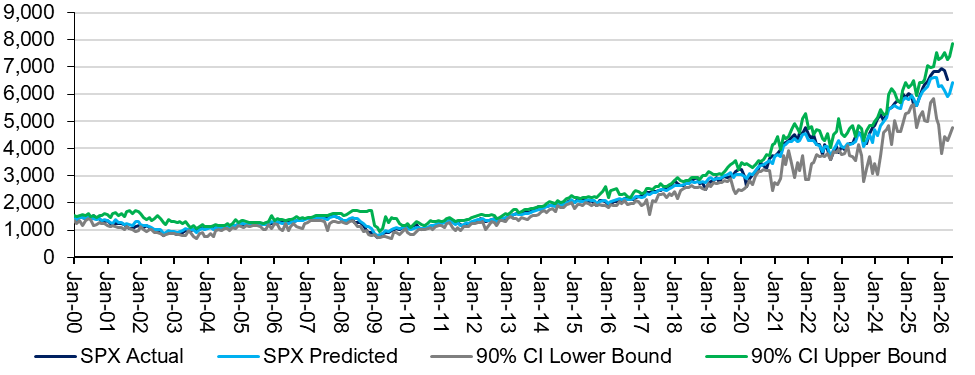

Multifactor Macro Market Model has been suggestive of March 2026 softness, rebound. Optimal’s Multifactor Macro Market Model projects the S&P 500 as well as bull and bear cases based on lagged data for 12 macroeconomic factors. The model suggested the S&P 500 to fall to just below 6000 by March, before rebounding back up to 6400 by May. We use this model as a guide to how macro would guide the market, given our analysis of current variables. This is, of course, outside of other factors at work. See Fig 17-18.

Figures 1-2: Optimal Advisory Consumer Velocity Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Consumer Spending y/y Relative to Historical Average

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Figures 3-6: Housing Kinetic Energy

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Mortgage Rates, For Sale Inventory, & Median List Price y/y Relative to Historical Averages (Since 2020)

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Figures 7-8: Gas Prices y/y

Source: Optimal Advisory Analysis, Bloomberg

Gas Prices y/y Relative to Historical Averages (Since 1992)

Source: Optimal Advisory Analysis, Bloomberg

Figures 9-12: Consumer Sentiment T3M and T9M y/y

Sentiment y/y by Income Tercile Relative to Historical Averages

Comparison of Sentiment y/y Across Income Terciles

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Figures 13-16: Consumer Wealth Effect & Components y/y

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Median Home Price y/y, S&P 500 y/y, & Wealth Effect Index (Since 2022)

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Figures 17-18: Optimal Advisory Multifactor Macro Market Model

Historical Test Predictions vs. Actual (On Test Data Only)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 (Including Training & Test Data) with Confidence Intervals

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

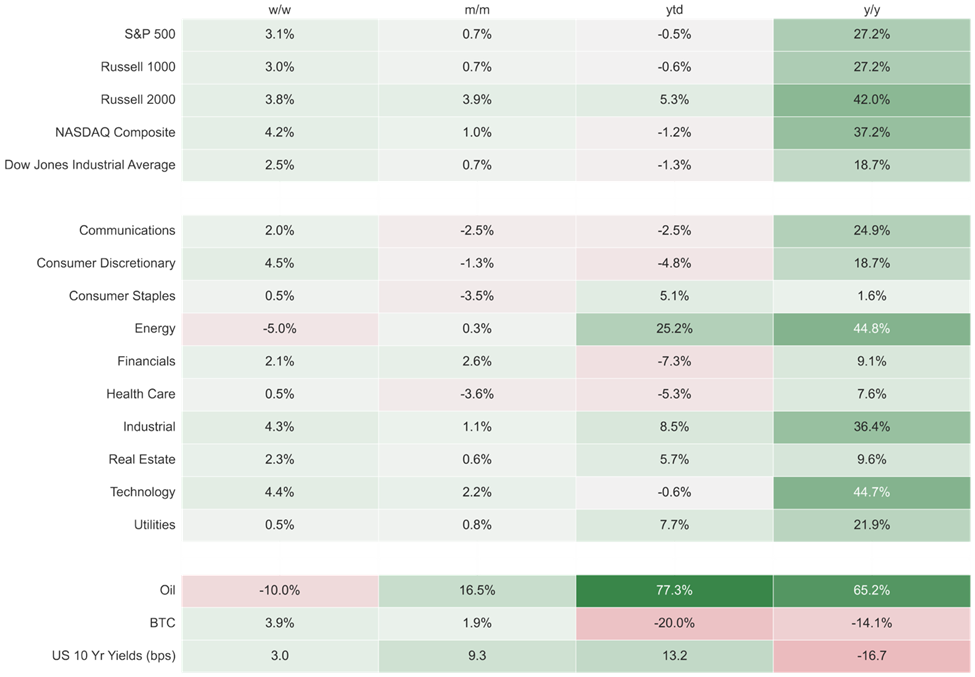

Figure 19: Index & Sector Performance

Source: Optimal Advisory Analysis, Bloomberg, prices at intraday 4/13/2026