Consumer Velo Stabilized, But at Meaningfully Soft Level Last Week; Notable Healthcare Services Drag to Spending; Gas Price Declines Become More Measurable: Macro Monday

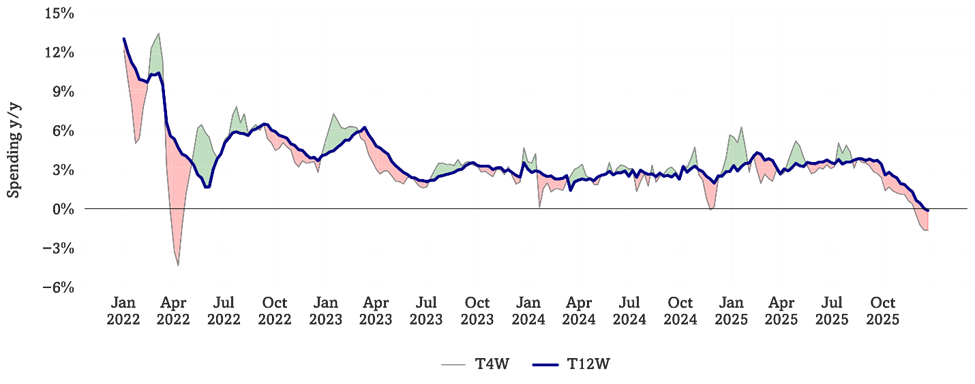

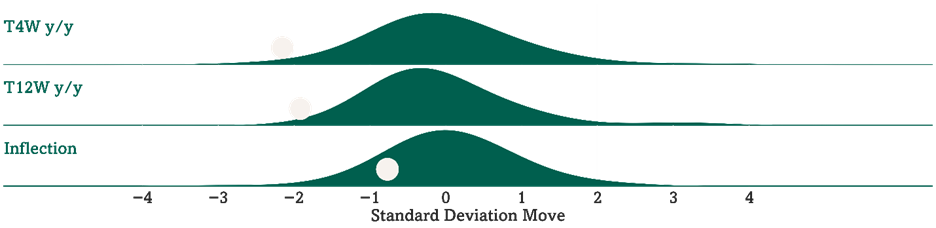

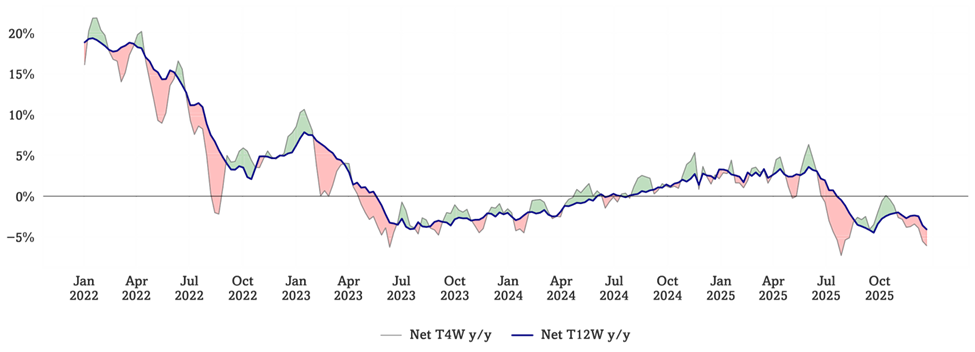

Consumer Velo soft again, but the softening is stabilizing a bit … shorter-term spending declines at -1.7% y/y (this metric was running +4% in August and +3% in September) while longer-term is now down -0.2% y/y. Our analysis of the trailing 4-week moving average of sales at 133 retailers and consumer concepts is running down -1.7% y/y (this is 2.2 standard deviations below average since the start of 2022). Consumer spending continues to be soft, but we note the slope is now flatter than it has been since early November. We are fielding questions about the strong PCE data in 3Q25 GDP that was released last week. We note (a) our analysis meaningfully softened starting in October and (b) healthcare was a significant contributor to PCE in the GDP print. At roughly 18% of PCE, healthcare service spending contributed a whopping 32% of PCE (or 76 bp of 3Q25’s PCE contribution of 239 bp to GDP total growth of 430 bp). The trailing Consumer Velo 12-week trend is down -0.2% y/y, leading to a shorter vs. longer-term inflection of -1.5% (0.8 standard deviations below average), the 18th straight week of shorter-term trends running below longer-term trends but a less negative inflection than the prior two weeks. See Fig 1-2.

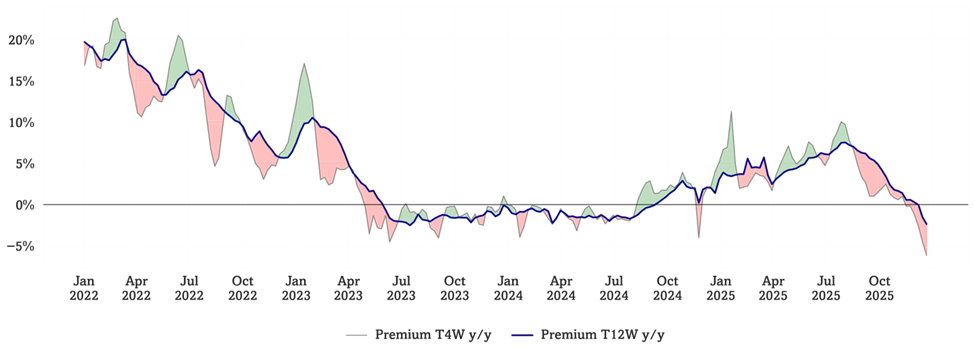

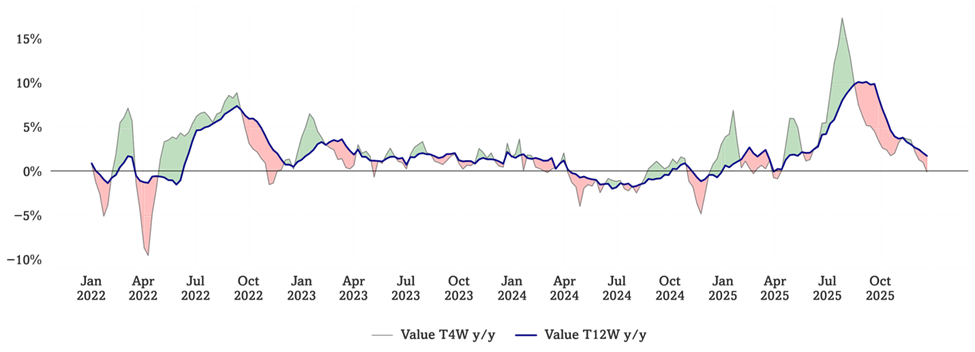

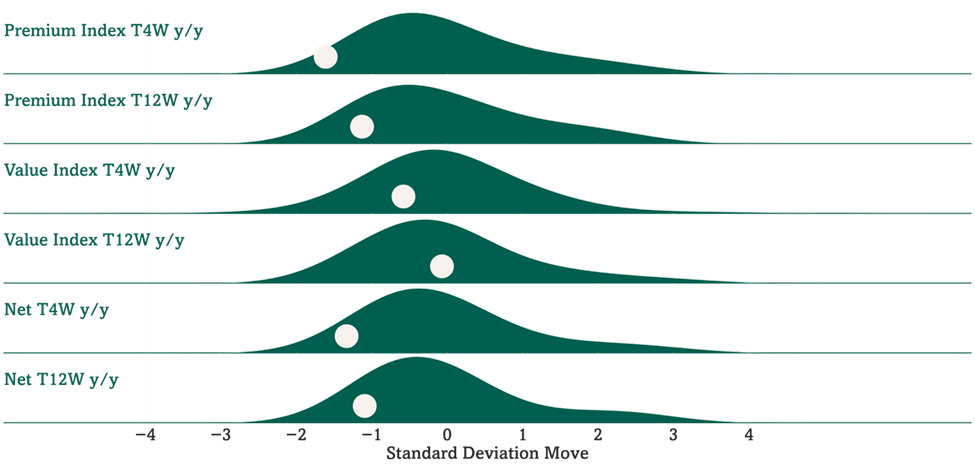

Our Premium Index is tracking softer than Value on a longer-term trend, softer spending trends in recent weeks are at the higher-end. We use a combination of consumer spending and psychographic monitoring to track “trade up” and “trade down” trends. Optimal’s premium monitor is running down -6.2% y/y on a T4W basis and down -2.4% y/y on a T12W basis, running 610 bp (1.3 standard deviations below average) and 410 bp (1.1 standard deviations below average) respectively below our Value Monitor, which is running down -0.1% y/y on a T4W basis and up 1.7% y/y on a T12W basis. See Fig 3-6.

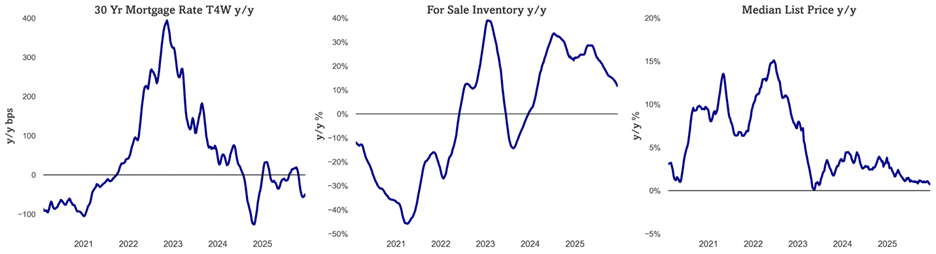

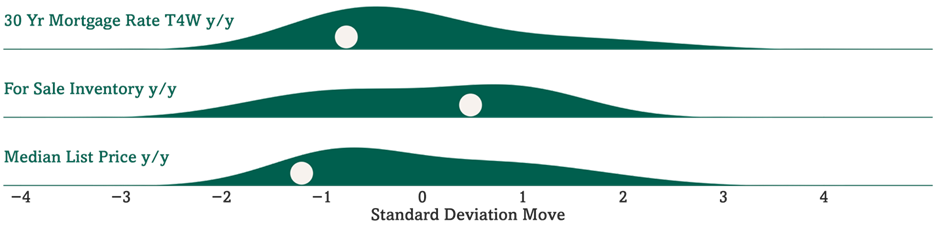

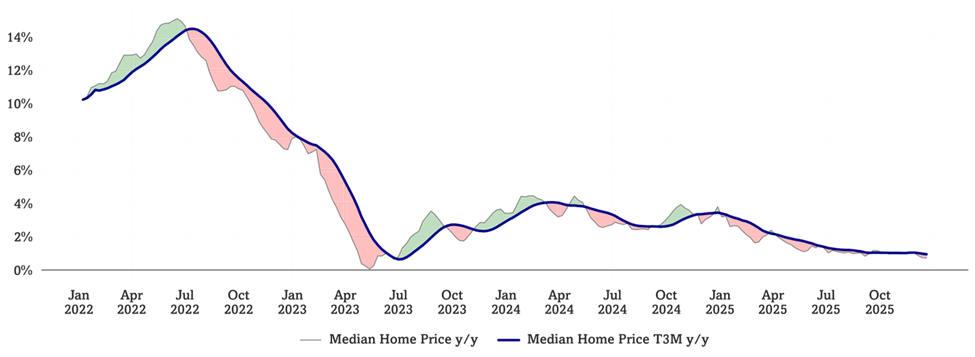

Consumer housing “kinetic energy” remains mixed; mortgage rates between 6-7% for all of 2025, with stable home prices nationally. For sale inventory running up +11.7% y/y (0.5 standard deviations above average) but at the lowest y/y level since early 2024. US 30Y FRM rate continues to run down, now running down -49bps y/y on a T4W basis. MBA’s mortgage applications for purchase are currently running +17% y/y. Median home prices are running up +0.7% y/y (1.2 standard deviations below average since 2020). Roughly 18% of Americans sell, build, fix, lend to, and furnish homes – velocity matters for the economy. See Fig 7-10.

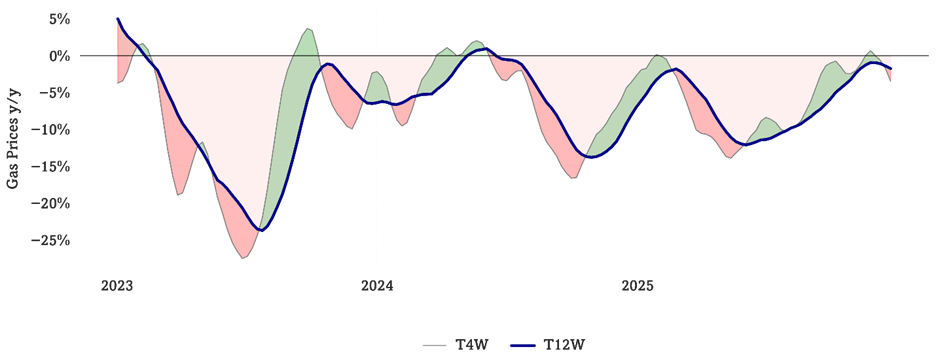

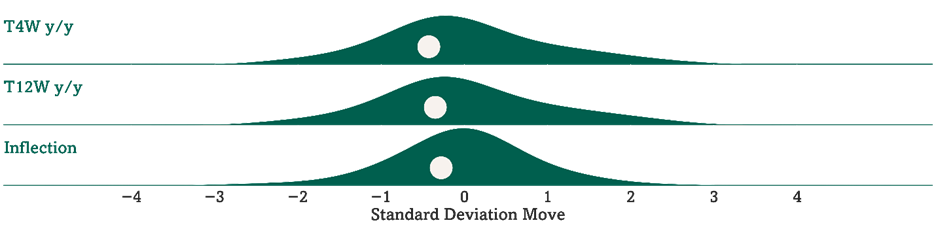

Gasoline price y/y declines are now more meaningful. Gas prices ran down -3.5% y/y on a T4W basis, the largest decline since September, after briefly turning positive y/y following 41 consecutive weeks of y/y declines through early November, and declined -1.8% y/y on a T12W y/y basis, corresponding to a -1.7% inflection between shorter and longer-term trends (approximately average relative to historical trends), the second week of negative inflections following 18 consecutive weeks of positive inflections and the most negative inflection since May. See Fig 11-12.

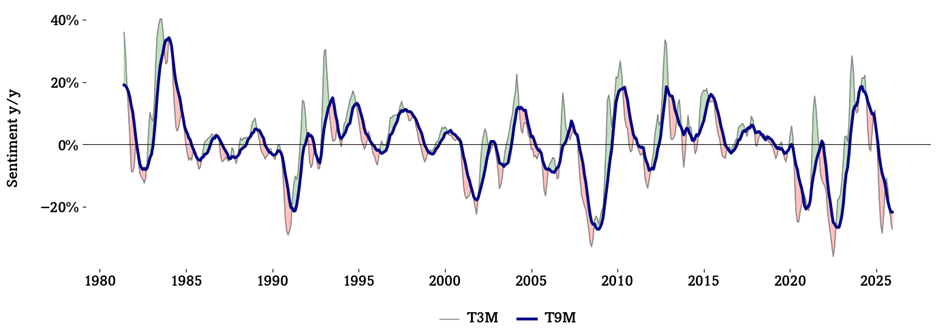

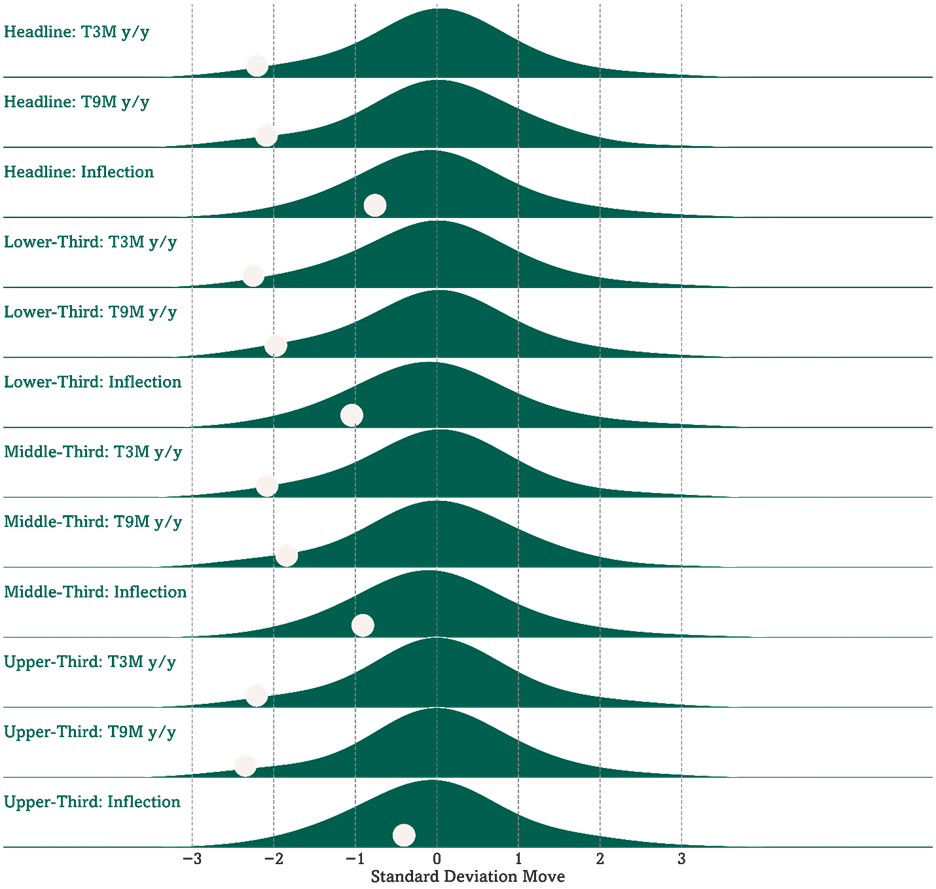

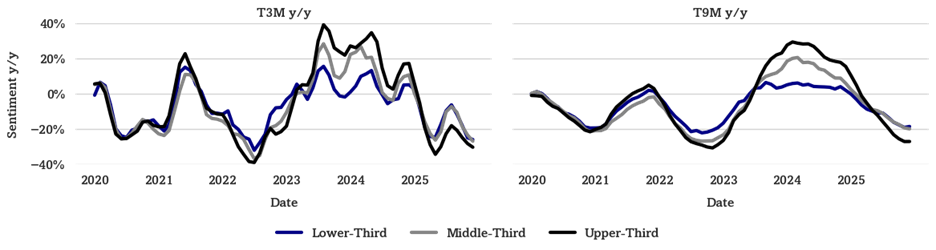

Consumer Sentiment at historically weak levels and the y/y trend is nearing 2025 lows on a shorter-term basis. Headline Sentiment has declined -27% y/y on a T3M basis (2.2 standard deviations below average) and -22% y/y on a T9M basis (2.1 standard deviations below average), marking the first month since late 2024 and second month since early 2024 where longer-term Sentiment y/y did not decrease from the prior month. Upper-third income Sentiment has declined -30% y/y on a T3M basis (2.2 standard deviations below average), middle-income Sentiment has declined -27% y/y on a T3M basis (2.1 standard deviations below average), and lower-income Sentiment has declined -26% y/y on a T3M basis (2.3 standard deviations below average). See Fig 13-16.

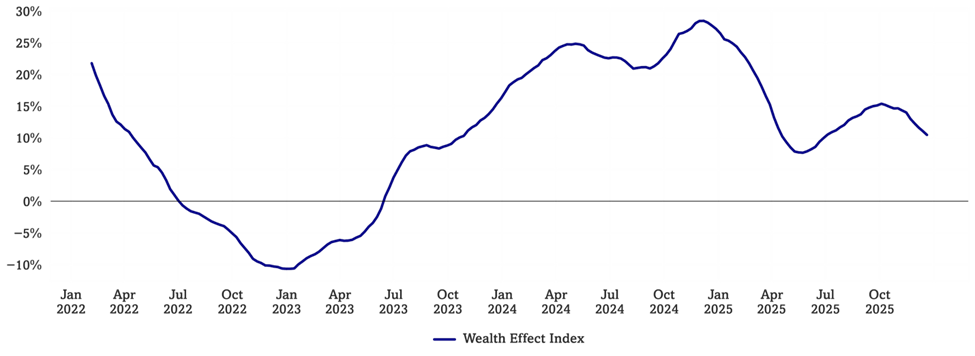

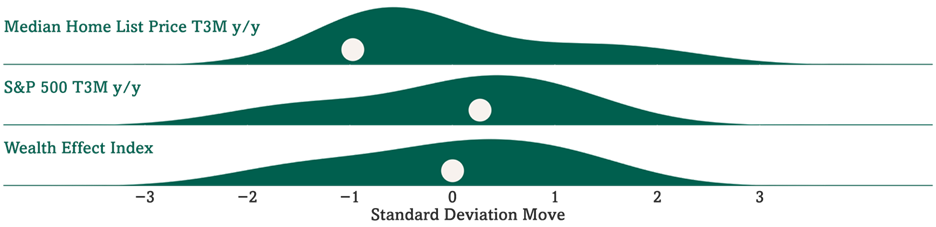

Consumer Wealth Effect Index has been softening in recent weeks, currently at average level. Optimal Advisory’s Wealth Effect Index is currently at 10.5% y/y (0.0 standard deviations above its mean value since the start of 2022) after peaking at 15.4% in early October. See Fig 17-20.

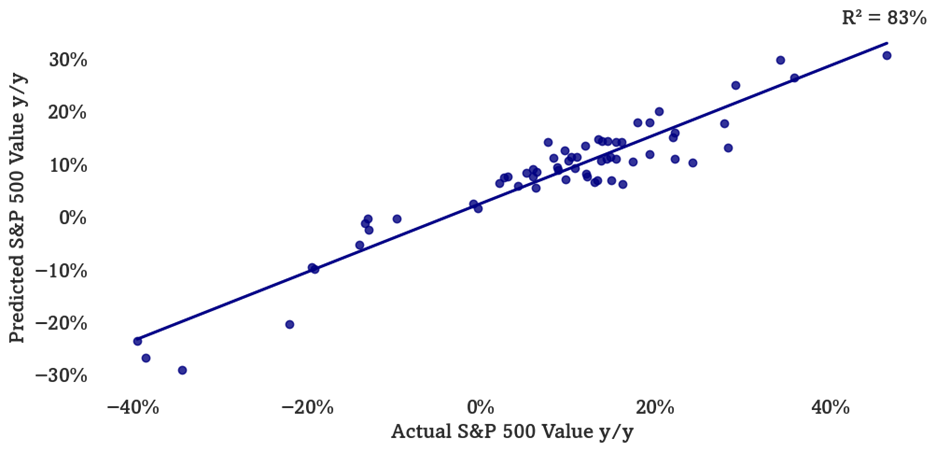

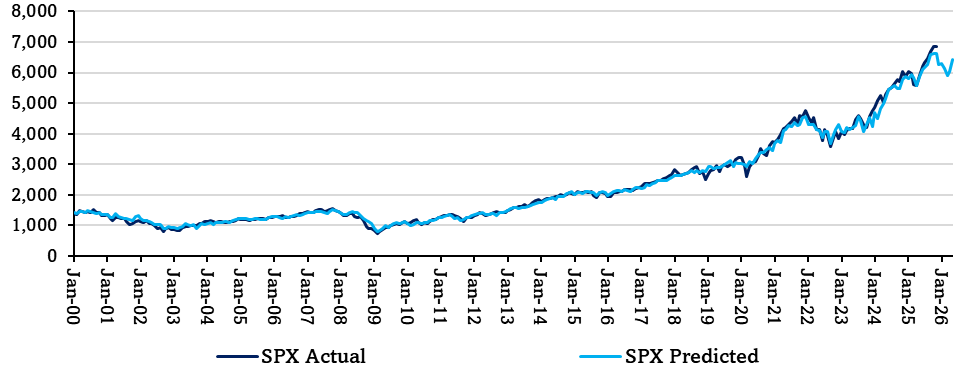

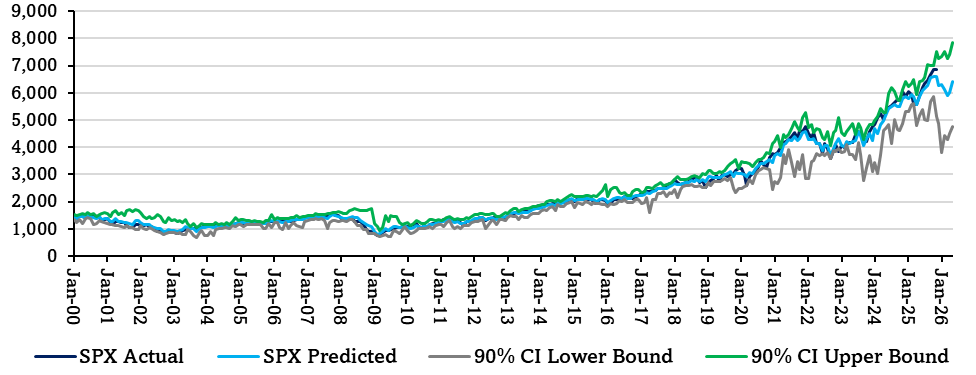

Multifactor Macro Market Model suggesting downturn, rebound. Optimal’s Multifactor Macro Market Model projects the S&P 500 as well as bull and bear cases based on lagged data for 12 macroeconomic factors. The model suggests the S&P 500 to fall to just below 6000 by next March, before rebounding back up to 6400 by May. See Fig 21-23.

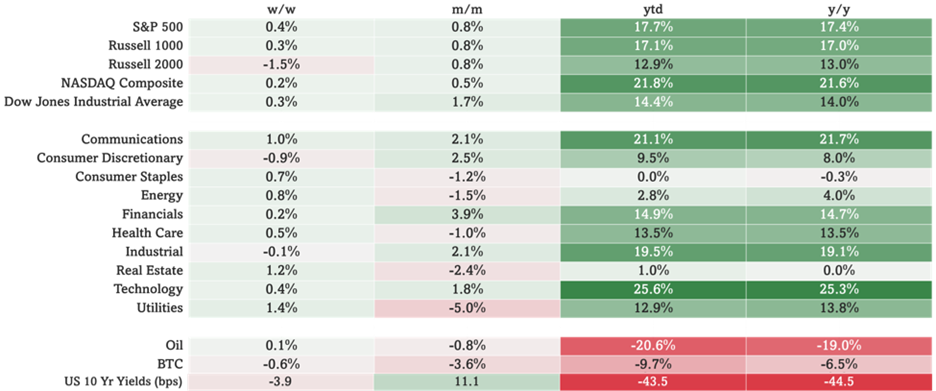

In this weekly note, we focus on key changes in the US consumer’s real-time dynamics (70% of the US economy). We also calculate and present the extent to which current dynamics are “non-normal”, relative to historic patterns. See Fig 24 for sector market performance.

Figures 1-2: Optimal Advisory Consumer Velocity Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Consumer Spending y/y Relative to Historical Average

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Figures 3-6: Optimal Advisory Premium vs Value Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure, Google Trends

Optimal Advisory Premium vs Value Indices Relative to Historical Averages

Source: Optimal Advisory Analysis, Bloomberg Second Measure, Google Trends

Figures 7-10: Housing Kinetic Energy

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Mortgage Rates, For Sale Inventory, & Median List Price y/y Relative to Historical Averages (Since 2020)

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Figures 11-12: Gas Prices y/y

Source: Optimal Advisory Analysis, U.S. Energy Information Administration

Gas Prices y/y Relative to Historical Averages (Since 1992)

Source: Optimal Advisory Analysis, U.S. Energy Information Administration

Figures 13-16: Consumer Sentiment T3M and T9M y/y

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Sentiment y/y by Income Tercile Relative to Historical Averages

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Comparison of Sentiment y/y Across Income Terciles

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Figures 17-20: Consumer Wealth Effect & Components y/y

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

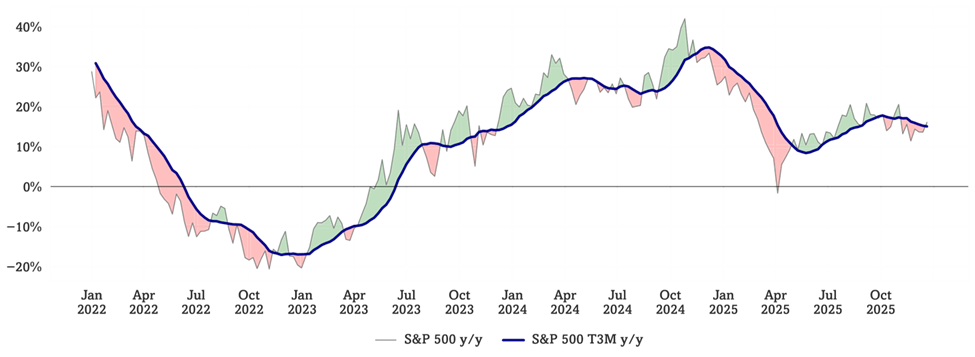

Median Home Price y/y, S&P 500 y/y, & Wealth Effect Index (Since 2022)

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Figures 21-23: Optimal Advisory Multifactor Macro Market Model

Historical Test Predictions vs. Actual (On Test Data Only)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 (Including Training & Test Data)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 with Confidence Intervals

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Figure 24: Index & Sector Performance

Source: Optimal Advisory Analysis, Bloomberg, prices intraday 12/29/2025