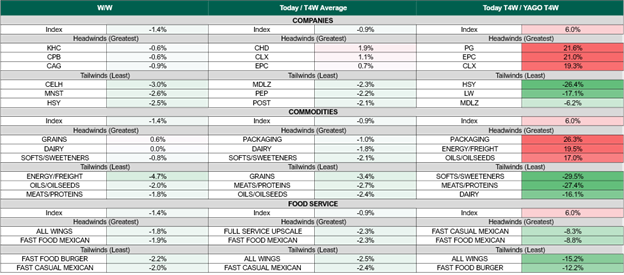

Costs Ease (-1.4% w/w, +6.0% y/y), Still a Shocking +17% Since Late February Led By Energy; HSY+, LW+, MDLZ+, PG-, EPC-, CLX-

The Optimal Advisory Cost Factor declined again this week and decelerated on a y/y basis for just the second time since the breakout of the Iranian conflict. The factor remains a headwind (+6.0% y/y) to CPG as tailwinds from softs, sweeteners, and non-beef proteins are being more than offset by packaging and energy headwinds. Restaurants, especially heavy chicken buyers (e.g. WING) are selectively enjoying margin tailwinds while the comp picture for retailers (e.g. KR, ACI, WMT) is mixed as major perishables categories including dairy, chicken & eggs are deflationary.

Cost tailwinds to watch: Softs/Sweeteners down -29.5% y/y (and at 12mo lows), Meats/Proteins –27.4% y/y, HSY -26.4% y/y, LW –17.1% y/y, MDLZ -6.2% y/y, Energy & Freight -4.7% w/w. See Fig 1.

Cost headwinds to watch: Packaging +26.3% y/y, Energy/Freight +19.5% y/y, PG +21.6% y/y, EPC +21.0% y/y. See Fig 1.

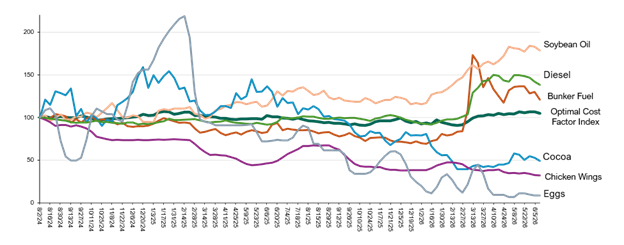

Higher energy costs & shipping risk are implicitly an immediate tax on everything: Within COGS, they drive the cost of packaging (esp. aluminum), inbound & outbound freight as well as farm level costs (diesel, fertilizer) that are key to plantings, supply & future food inputs. Within SG&A, they drive delivery costs. They also threaten revenue with more consumer budget constraints. We monitor weekly performance of key equity indices and macro indicators. See Fig 11.

Crude slides to two-month lows on a fading war-risk premium. WTI fell more than 4% toward $86 a barrel, it’s lowest since a brief low in April, after President Trump suspended planned attacks against Iran and signaled that Washington and Tehran were close to a deal. WTI has now declined 16% over the past four weeks.

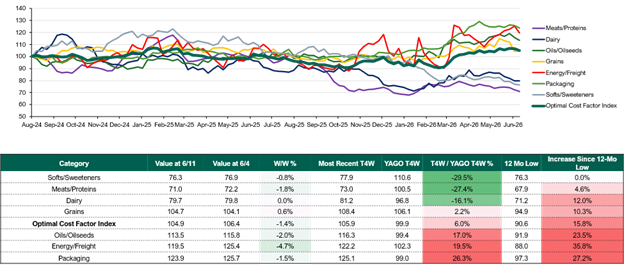

Cost Factor -1.4% w/w, +6.0% y/y (vs. prior week -0.1% w/w & +7.4% y/y). Notable commodity moves this week include Bunker Fuel -7% w/w, still up 74% ytd; Diesel -8% m/m, up +49% ytd; Eggs continue to test lows on excess supply: down -24% m/m, and -57% ytd.

In this weekly note, we identify spot input costs’ putative impact on the U.S. fast moving consumer goods (FMCG) value chain, most measurably impacting staples, staples retailers, restaurants & food service. Optimal’s proprietary cost factor weights ticker & sector specific cost trends using a proprietary formula based on 32 trackable spot cost inputs – 23 of which are updated as of last night, the other 9 are latest available.

Figure 1: Weekly Cost Factor Summary

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 2: Weekly Cost Factor Margin Context

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 3: Weekly Input Commodity Performance by Group

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 4: Biggest Input Cost Movers y/y

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 5: Food Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

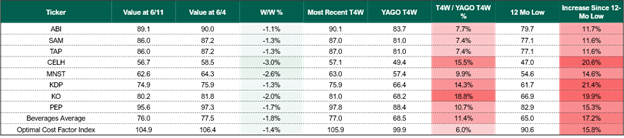

Figure 6: Beverage Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 7: HPC Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

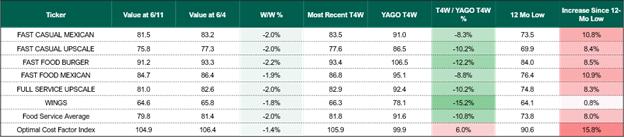

Figure 8: Restaurant Level Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

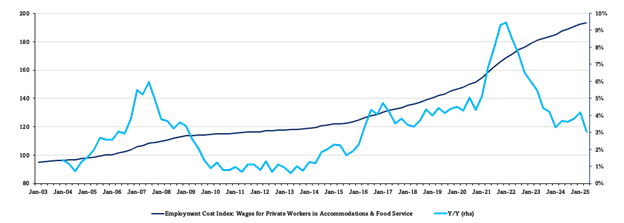

Figure 9: Restaurant Employment Cost Index

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

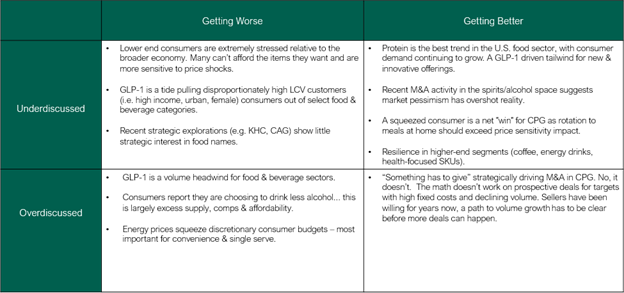

Figure 10: Staples Sector Theme Box

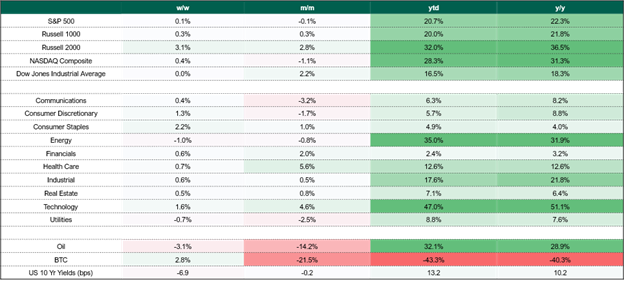

Figure 11: Market Sector Performance

Sources: Optimal Advisory Proprietary Analysis, Bloomberg