Input Costs -0.6% w/w, -12.0% y/y, Food Inputs Lead Decline. Oilseeds Jump. Friday Cost Factor.

Optimal Advisory Cost Factor – Cost Factor down w/w again this week and input costs continue to serve as tailwinds for Staples companies. The Optimal Cost Factor down (-0.6% w/w) and remains down sharply (-12.0%) y/y.

Lower Input costs do a few things:

- Help restaurant (YUM, DRI, CMG, CAVA) margins and/or provide fuel for traffic driving spend promotions – which is especially timely given the rising importance of protein.

- Usually improve the economics of protein value chains generally (JBS, HRL, SFD, TSN) because end market pricing is stickier than upstream costs (e.g. feed).

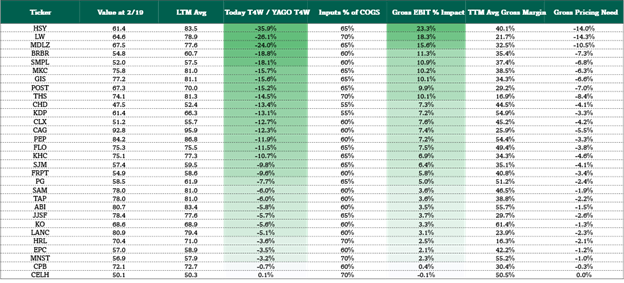

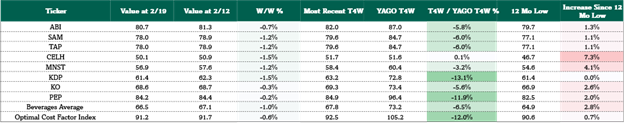

- Give a measurable H1 EPS tailwind to otherwise challenged CPG companies (HSY, MDLZ most) relative to planning period (early fall) expectations. See Fig 2.

- Challenge H1 2026 grocery comp both in perishables (KR, ACI) and stoking “select” price cuts (e.g. private label) as they chase traffic. It’s also partially what’s fueling “select” price cuts for center store CPG – which are getting less “select” by the day.

- Enhance center store grocery wallet through lower perishables spend (e.g. milk, meat, eggs), where input costs pass through directly.

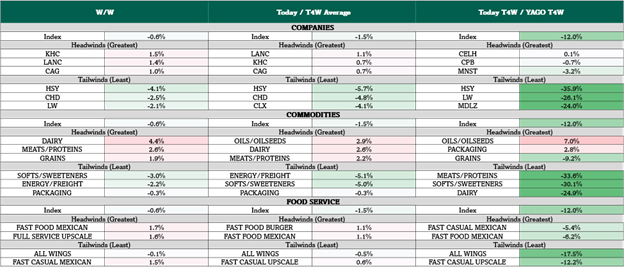

Cost tailwinds to watch: Meats/Proteins down -33.6% y/y, HSY -35.9% y/y, LW -26.1% y/y, Wing restaurants -17.5% y/y. See Fig 1.

Cost headwinds to watch: Oil/oilseeds +7.0% y/y, Packaging +2.8% y/y, CELH +0.1% y/y. See Fig 1.

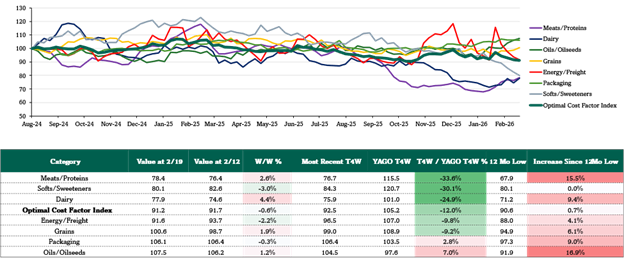

Changes at the largest cost tailwinds & headwinds, especially among food inputs. Soybean oil has moved higher (+27.8% y/y) to lead measured commodities. Oils/Oilseed the leading commodity category in terms of headwinds, running up +7.0% y/y, and up +16.9% from 12-mo low. Meats/Proteins (-33.6% y/y) and Softs/Sweeteners (-30.1% y/y and currently at 12-mo low) continue to be the greatest beneficiary of lower input costs as Eggs & Cocoa are both down more than -60% y/y. Direct translation to food producers, as average input cost index for constituents down -13.8% y/y, ahead of beverages (-6.8% y/y), HPC (-9.3% y/y), and food service (-9.6 % y/y). See Fig 5-8.

Cost Factor -0.6% w/w, -12.0% y/y (vs. prior week -1.3% w/w & -10.7% y/y).

Energy volatility continues to unwind as natural gas down -41.0% m/m, paired with continued lower costs for coca; cost factor trending lower w/w for 4 consecutive weeks. Input costs down double-digits y/y since mid-January.

In this weekly note, we identify spot input costs’ putative impact on the U.S. fast moving consumer goods (FMCG) value chain, most measurably impacting staples, staples retailers, restaurants & food service. Optimal’s proprietary cost factor weights ticker & sector specific cost trends using a proprietary formula based on 32 trackable spot cost inputs – 23 of which are updated as of last night, the other 9 are latest available.

Figure 1: Weekly Cost Factor Summary

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 2: Weekly Cost Factor Margin Context

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 3: Weekly Input Commodity Performance by Group

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

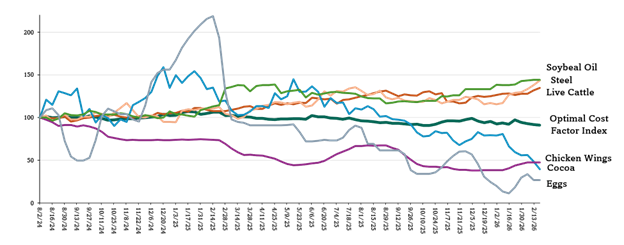

Figure 4: Biggest Input Cost Movers y/y

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 5: Food Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 6: Beverage Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 7: HPC Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 8: Restaurant Level Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

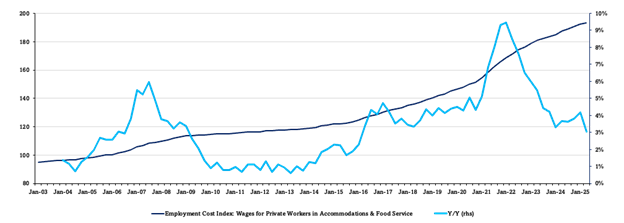

Figure 9: Restaurant Employment Cost Index

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

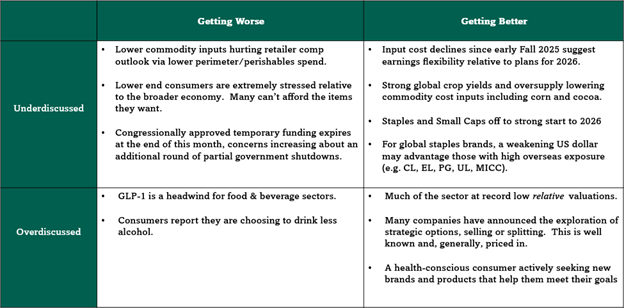

Figure 10: Staples Sector Theme Box

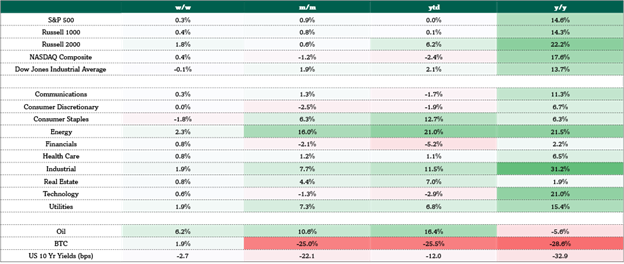

Figure 11: Market Sector Performance

Sources: Optimal Advisory Proprietary Analysis, Bloomberg