Input Costs +3.3% w/w, -9.2% y/y, Energy & Freight Costs Popping, But Inputs Still Tailwind. Friday Cost Factor. HSY+, LW+, Beverages-, HPC-

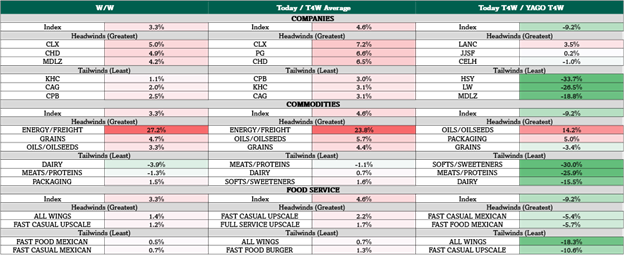

The Optimal Advisory Cost Factor jumped again this week (+3.3% w/w) but remains down (-9.2% y/y), driven by energy & freight costs in the wake of Middle East conflict. Fertilizer supply uncertainty is a rising concern at the farm level.

Cost tailwinds: Softs/Sweeteners down -30.0% y/y, HSY -33.7% y/y, LW -26.5% y/y, Wing restaurants -18.3% y/y. See Fig 1.

Cost headwinds: Energy/Freight +27.2% w/w, Oil/Oilseeds +14.2% y/y, LANC +3.5% y/y. See Fig 1.

Higher Energy/Freight Costs with broad-reaching exposure to Staples. Oil up +50% m/m. For the second week in a row; all 30/30 measured company specific costs factor indices up w/w (along with 6/6 food service indices). See Fig 5-8.

Higher energy costs & shipping risk are a implicitly an immediate tax on everything:

- Within COGS, they drive the cost of packaging (esp. aluminum), inbound & outbound freight as well as farm level costs (diesel, fertilizer) that are key to plantings, supply & future food inputs.

- Within SG&A, they drive delivery costs for manufacturers, distributors and staples retailers.

- Gasoline prices also threaten revenue with fewer trips, C-Store sticker shock & consumer budget constraints. We monitor weekly performance of key equity indices and macro indicators. See Fig 11.

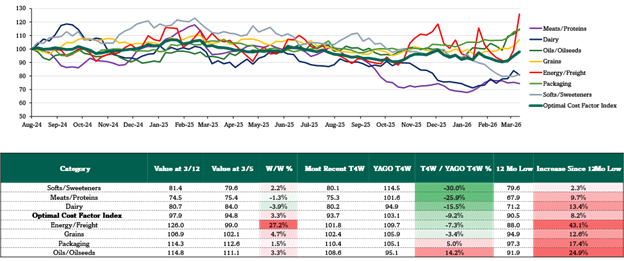

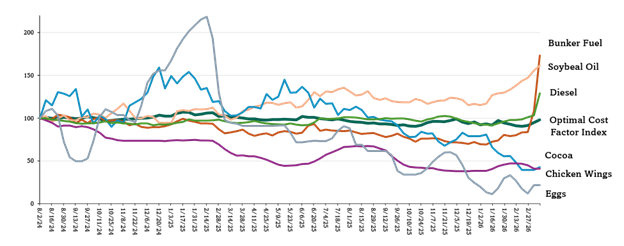

We note continued input commodity tailwinds for Softs/Sweeteners & Proteins exposed companies. HSY & MDLZ lead measured companies in gross EBIT impact from lower input costs (specifically cocoa, down -45%. See Fig 2. We also note continued lower prices from poultry products such as eggs & wings (see Fig 4) continuing to benefit from protein (ex. beef) tailwinds (-25.9% y/y). See Fig 3.

Cost Factor +3.3% w/w, -9.2% y/y (vs. prior week +1.9% w/w & -12.5% y/y). Every spot energy inputs higher this week. Most notably – Bunker Fuel +60% w/w, and up +148% YTD; Diesel +25% w/w, +39% ytd & +34% y/y). These could not have been part of budgets set last fall…or last month.

In this weekly note, we identify spot input costs’ putative impact on the U.S. fast moving consumer goods (FMCG) value chain, most measurably impacting staples, staples retailers, restaurants & food service. Optimal’s proprietary cost factor weights ticker & sector specific cost trends using a proprietary formula based on 32 trackable spot cost inputs – 23 of which are updated as of last night, the other 9 are latest available.

Figure 1: Weekly Cost Factor Summary

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 2: Weekly Cost Factor Margin Context

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 3: Weekly Input Commodity Performance by Group

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 4: Biggest Input Cost Movers y/y

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 5: Food Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 6: Beverage Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 7: HPC Sector Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

Figure 8: Restaurant Level Cost Factor

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

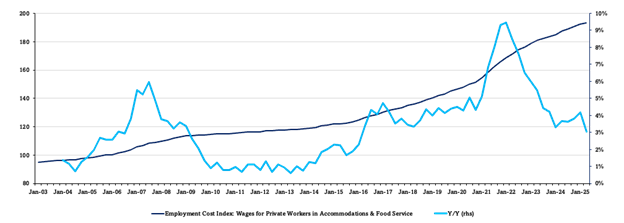

Figure 9: Restaurant Employment Cost Index

Sources: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, USDA, BEA

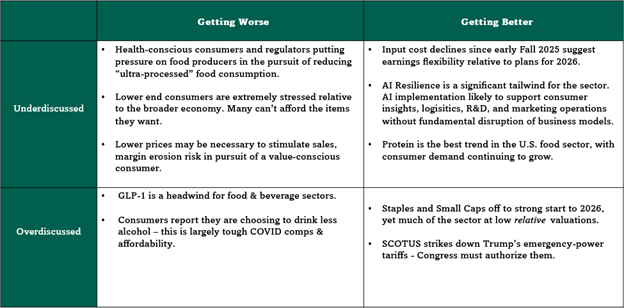

Figure 10: Staples Sector Theme Box

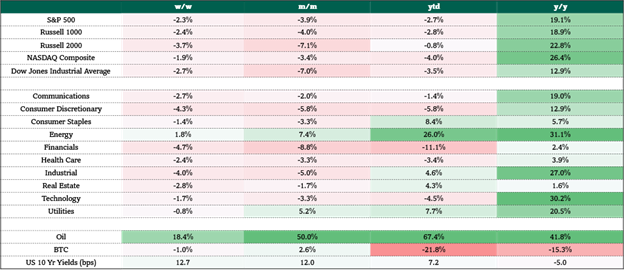

Figure 11: Market Sector Performance

Sources: Optimal Advisory Proprietary Analysis, Bloomberg