Intriguing Jump in Pending Home Sales & What Could it Mean; Gasoline Up and Sentiment Down: Macro Monday

Summary: (1) Consumer spending remained in general subdued trend last week as the T4W trend lifted to +1.4% y/y (from +1.1% the prior week) while the 12-week trend decelerated slightly to +2.6% y/y (from +2.8% the prior week), with the gas pump still mostly responsible, see Fig 1; (2) Mortgage rates moved a touch lower on the week (30Y FRM at 6.36%) but housing remains effectively frozen but we note a significant jump in pending home sales, see Chart of the Week and Fig 3-6; (3) Gasoline prices +73% y/y with the T4W trend at +70%, now past the 6-8 week window we have discussed where any sustained pressure historically reshapes consumer behavior, see Fig 7; (4) Lower- and middle-income Sentiment remained near all-time lows while upper-third Sentiment has stabilized as equities have performed such that the Wealth Effect Index posted its seventh consecutive weekly gain, see Fig 12-16. Optimal is hosting our Wine & Spirits Summer Preview virtual client meeting Thursday 5/21 at 10:30 am ET, Register for Meeting Here.

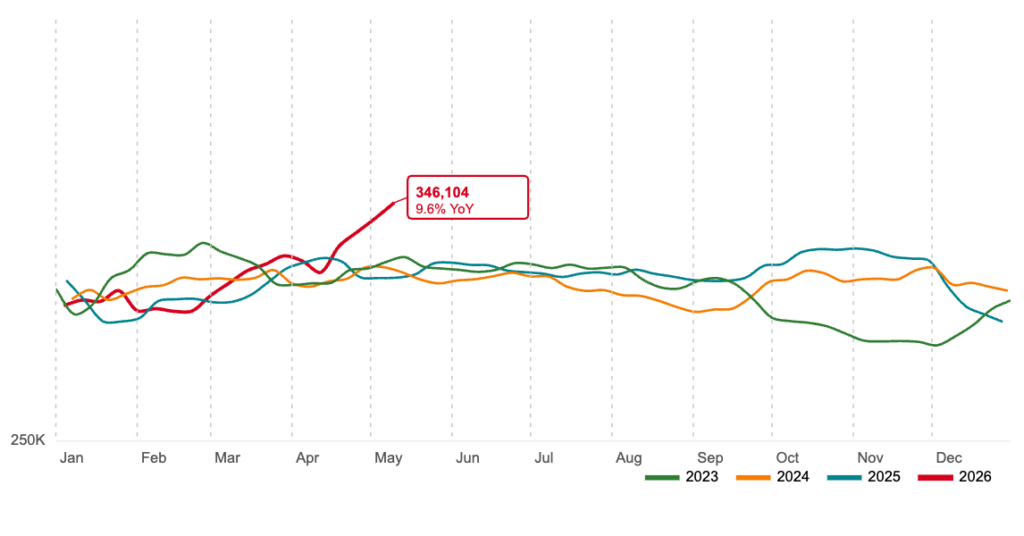

Chart of the Week: Jumping Pending Home Sales y/y

Sources: Optimal Advisory Analysis, Redfin data

The Pending Home Sales Jump … In the last few weeks, pending home sales have broken out of their typical pattern of the last few years. Higher home prices, weak Sentiment, and higher mortgage rates have essentially frozen transactions since 2H23. At some point, though, households do buy and sell more (whether pent-up need or easy compares, or both). Until the last few weeks, transactions have remained near the level of April/May 2020 Covid lows (and 35% below 2018-2019, 17% below 2021-2022 post Covid jump). We estimate 18% of the economy is tied to building, fixing, furnishing, selling, and lending around home transactions. Home improvement and home furnishing categories benefit twice from transaction volume (sellers and buyers doing projects on the way out of and into homes). We continue to monitor this trend – a continuation could have impact on the economy and CY27 and CY28 Street estimates for home-related demand.

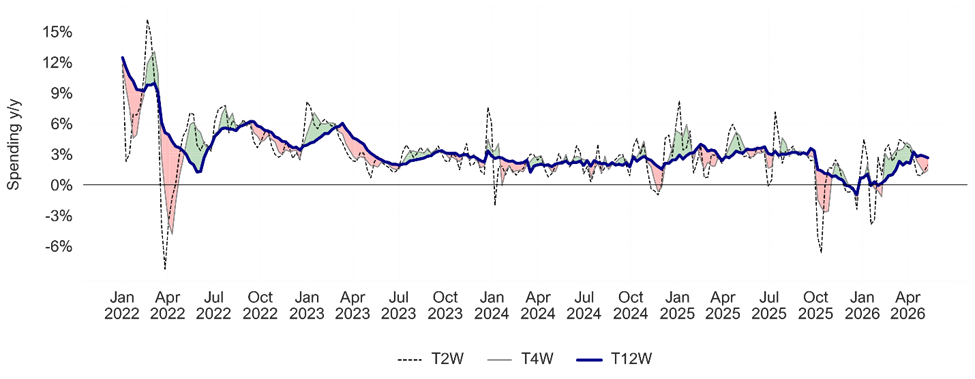

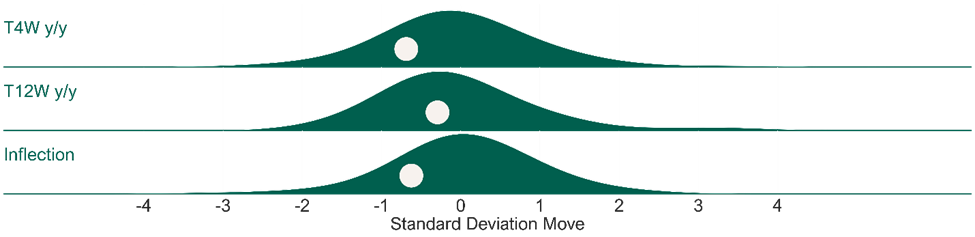

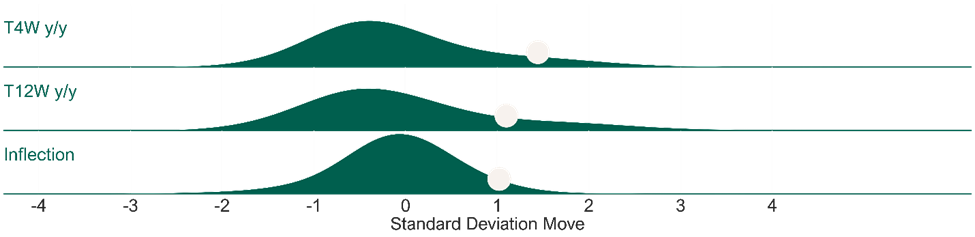

Our Consumer Velocity tracker improved modestly off last week’s low, up +1.4% y/y T4W following +1.1% y/y the prior week, though the T12W trend decelerated slightly to +2.6% y/y (from +2.8%). The underlying trend remains slightly soft (0.3 standard deviations below the post-2022 average on T12W and 0.7 standard deviations below on T4W). With gasoline spending continuing to inflate at the pump (prices +73% y/y), unit demand at gas stations remains pressured and that means trip consolidation. The T4W vs. T12W Inflection was -1.2 pts, the fourth consecutive week of shorter-term growth lagging longer-term. See Fig 1-2.

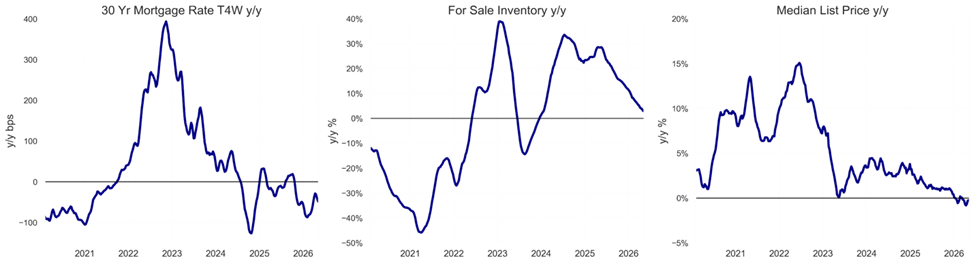

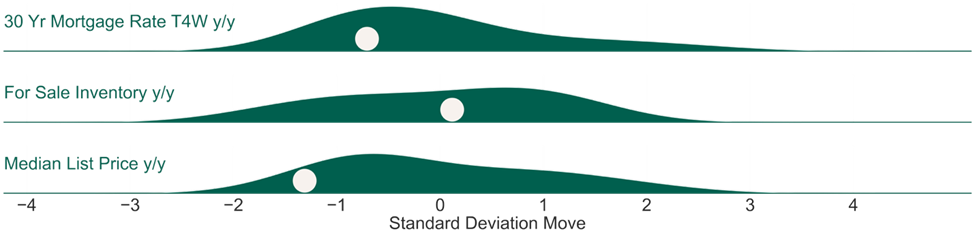

Housing activity remains virtually frozen but some positive inflection in precursor metrics. US 30Y FRM rate up to 6.36% running down -47 bps y/y on a T4W basis (0.7 standard deviations below average since 2020). MBA’s mortgage applications for purchase running up 5% y/y while refinance applications running up 29%. Median home prices are flat y/y (1.4 standard deviations below average since 2020). Roughly 18% of US GDP is related to the selling, building, fixing, lending to, and furnishing of homes – velocity matters for the economy. See Fig 3-6.

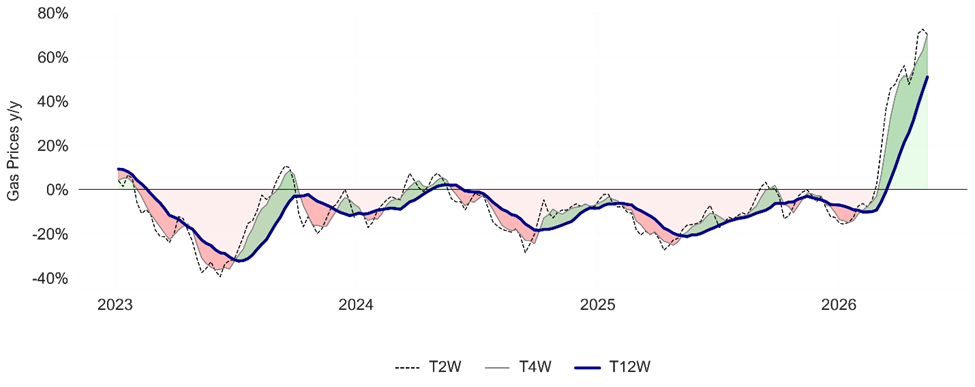

Gasoline inflation remains the dominant macro signal as the latest weekly print is up +73% y/y, with the T4W now at +70% y/y and the T12W at +51% y/y. The T4W reading is 1.4 standard deviations above average and we are now firmly in the 6-8 week window in which history suggests sustained price pressure begins to materially change consumer spending behavior. We continue to flag that utilities (electricity and heating fuel) run about 9% of lower-income household spending vs. 4% for higher-income households – compounding the squeeze at the bottom of the income distribution. See Fig 7-8.

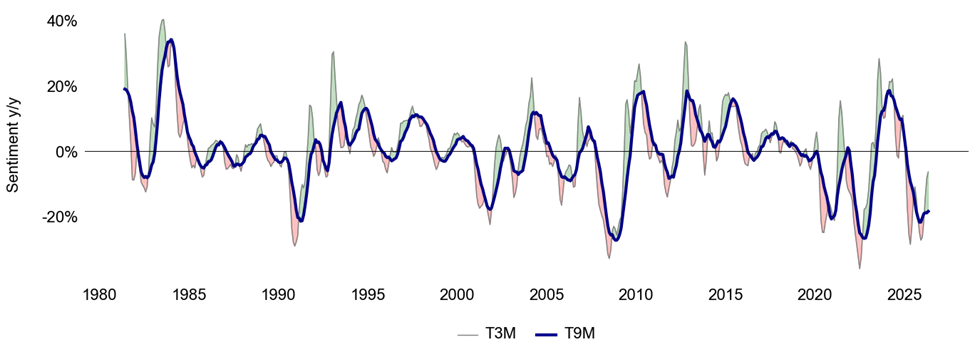

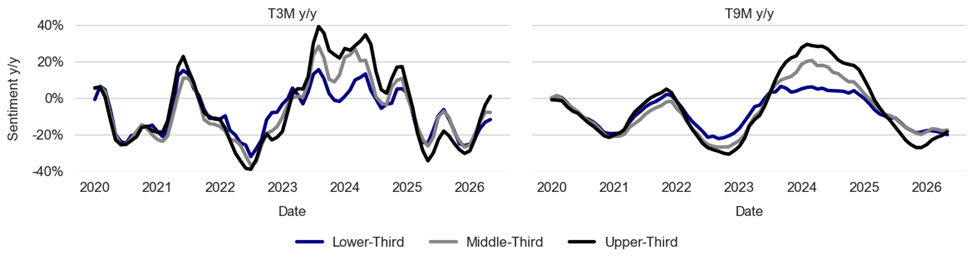

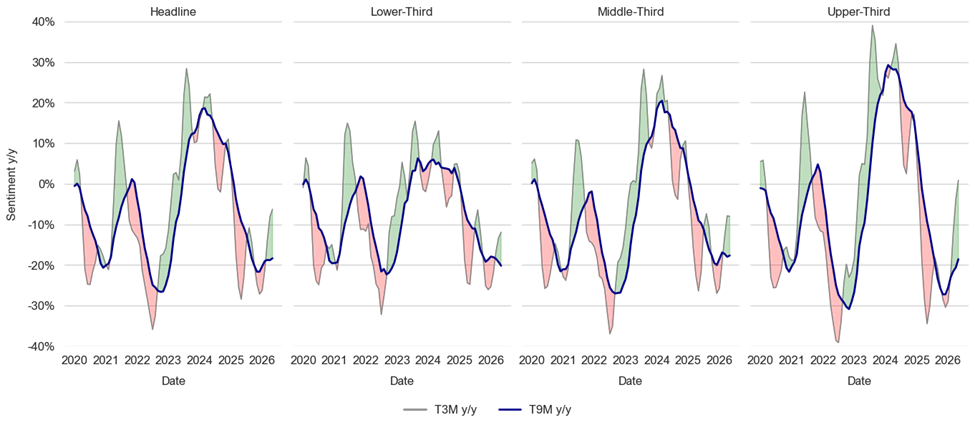

Sentiment is at all-time lows (currently at 48.2) for the second consecutive month, down -8% y/y this month despite lapping exceedingly weak comparisons. Overall, headline Sentiment is down -8% y/y this month alone and down -6% on a T3M basis (0.5 standard deviations below average) and -18% y/y on a T9M basis (1.7 standard deviations below average). Upper-third income Sentiment is up +1% y/y on a T3M basis (approximately average), after declining -4% y/y T3M last month. Middle-income Sentiment has declined -8% y/y on a T3M basis (0.6 standard deviations below average) each of the last two months, and lower-income Sentiment has declined -12% y/y on a T3M basis (1.0 standard deviations below average) compared to -13% last month. See Fig 9-12.

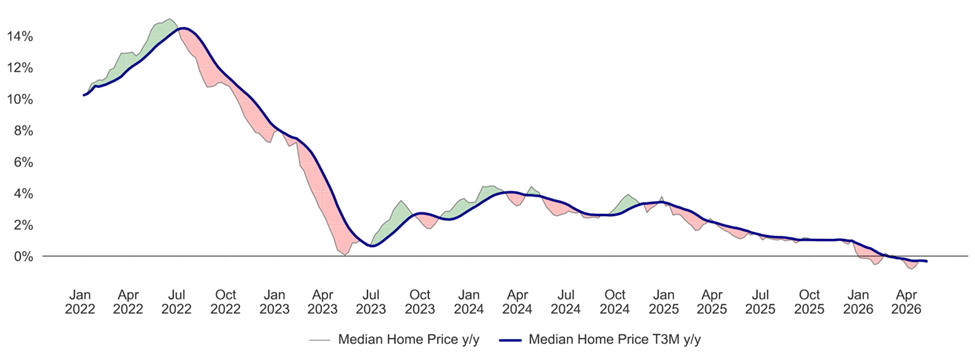

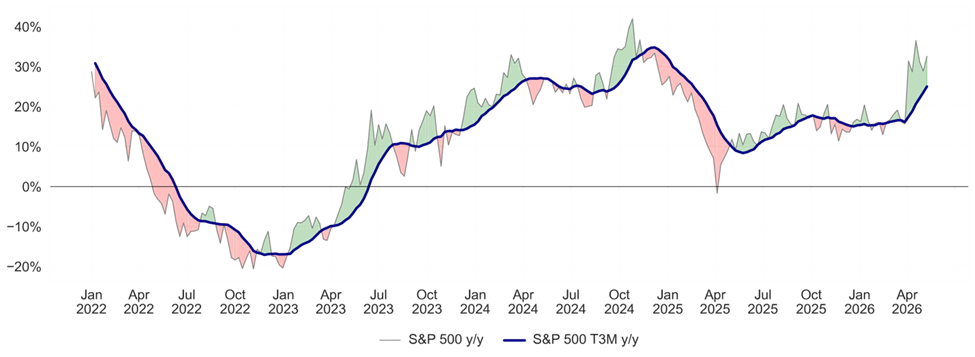

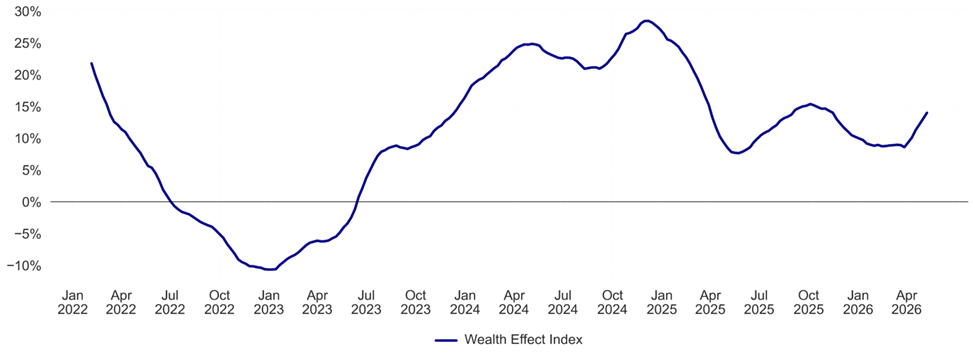

Consumer “Wealth Effect” continued momentum carried by equity returns. Optimal Advisory’s Wealth Effect Index is at +14.5% y/y (0.2 standard deviations above average since the start of 2022 and higher for 7 consecutive weeks). Equity returns have been strong, shrugging off conflict in the Middle East and higher energy prices, while beginning to lap a softer market from Spring 2025. With home prices flat y/y we note the “flywheel” of wealth effect turning higher. See Fig 13-16.

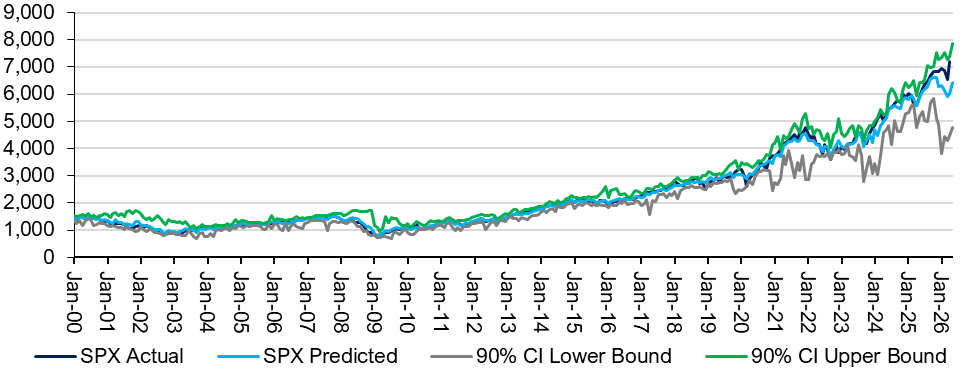

Our Multifactor Macro Market Model has been suggestive of March 2026 softness, rebound. Optimal’s Multifactor Macro Market Model projects the S&P 500 as well as bull and bear cases based on lagged data for 12 macroeconomic factors. The model suggested the S&P 500 to fall to just below 6000 by March, before rebounding back up to 6400 by May. We use this model as a guide to how macro would guide the market, given our analysis of current variables. This is, of course, outside of other factors at work. See Fig 17-18.

Figures 1-2: Optimal Advisory Consumer Velocity Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Consumer Spending y/y Relative to Historical Average

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Figures 3-6: Housing Kinetic Energy

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Mortgage Rates, For Sale Inventory, & Median List Price y/y Relative to Historical Averages (Since 2020)

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Figures 7-8: Gas Prices y/y

Source: Optimal Advisory Analysis, Bloomberg

Gas Prices y/y Relative to Historical Averages (Since 1992)

Source: Optimal Advisory Analysis, Bloomberg

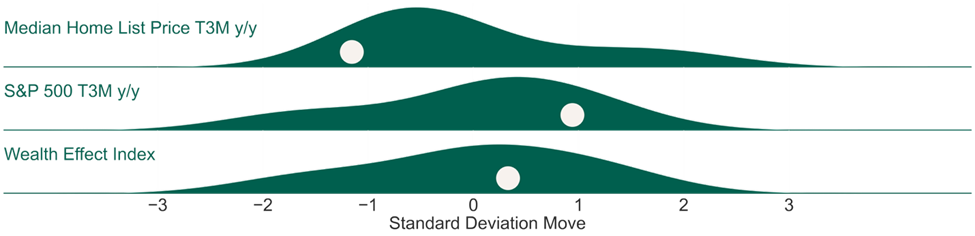

Figures 9-12: Consumer Sentiment T3M and T9M y/y

Sentiment y/y by Income Tercile Relative to Historical Averages

Comparison of Sentiment y/y Across Income Terciles

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Figures 13-16: Consumer Wealth Effect & Components y/y

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Median Home Price y/y, S&P 500 y/y, & Wealth Effect Index (Since 2022)

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Figures 17-18: Optimal Advisory Multifactor Macro Market Model

Historical Test Predictions vs. Actual (On Test Data Only)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 (Including Training & Test Data) with Confidence Intervals

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

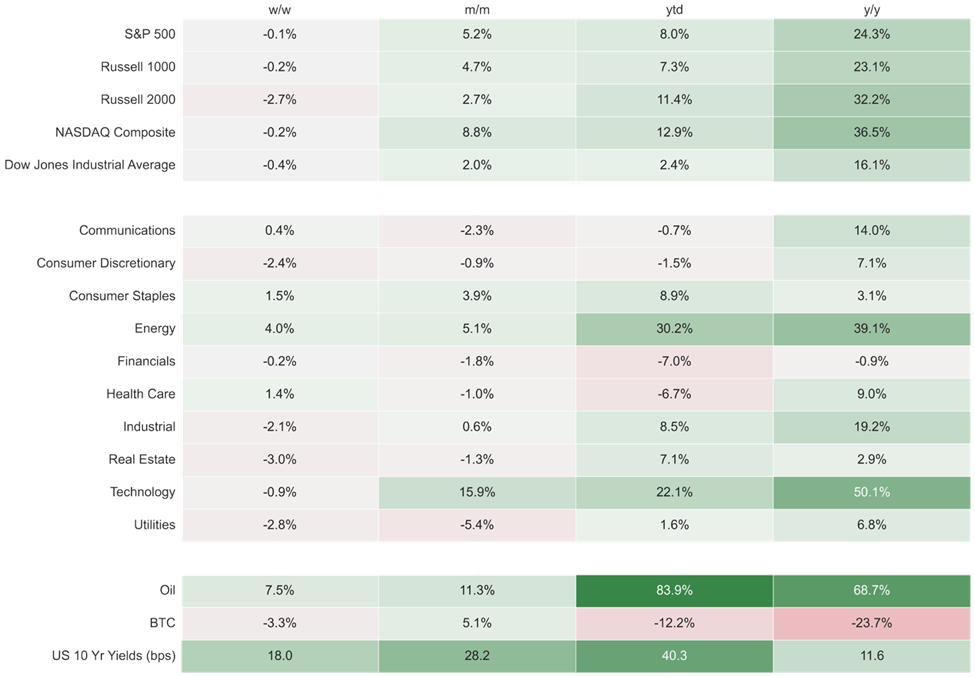

Figure 19: Index & Sector Performance

Source: Optimal Advisory Analysis, Bloomberg, prices at intraday 5/18/2026