Macro Monday: Fuel Price Math Updates, Value Outpacing Premium, Housing Market Checks

1) As we noted last week, the middle 3 income quintiles do about 5% of their spending on gasoline. So our 3-decade simple rule-of-thumb remains in place – that any 10% y/y move, then, creates a 50 bp headwind or tailwind to spending. Right now, that implies more than half of the spending growth we are tracking would be pressured if current conditions persist, see below.

2) Consumers respond to both magnitude and duration of external impacts like gas prices, jobs, and interest rates.

3) The current mix of (a) AI cited job losses; (b) fuel price and interest rate spikes from the current Iran conflict; and (c) friction from tariff headwinds, then strike down, and then replacement is formidable for Consumer Discretionary. At the same time, Jonathan Feeney’s work on relative “AI Resilience” highlights the strengths in and within Consumer Staples.

4) We are hosting a virtual meeting on hyper local AI build for agentic commerce, devices and sports/entertainment this Friday 3/13 at noon ET. Register

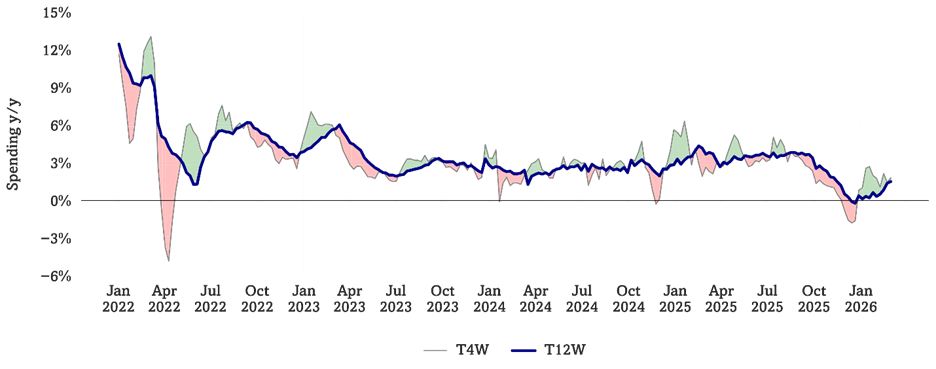

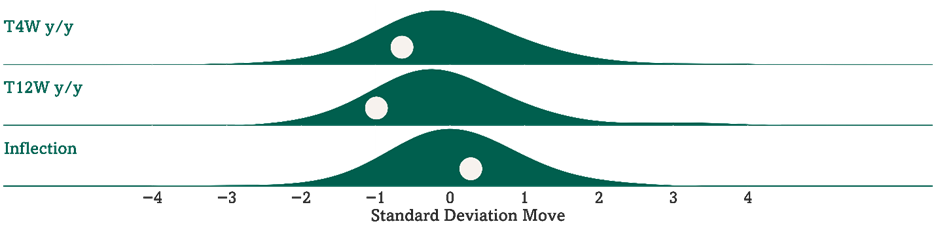

We are heading into fuel price shocks from a somewhat muted pace of consumer activity. Our Consumer Velocity tracker remained positive but soft, running up +1.8% y/y T4W (we note this data is through 3/1 and Consumer Velocity decelerated to flat y/y just for that week). This metric was running -1.6% y/y in mid-December but was up +3-4% in 3Q25. Our analysis of the trailing 4-week moving average of sales at 133 retailers and consumer concepts is running up +1.8% y/y (0.6 standard deviations below average since the start of 2022). The trailing Consumer Velo 12-week trend is up +1.5% y/y (1.0 standard deviations below average) vs. +1.4% y/y the prior week, leading to a shorter vs. longer-term inflection of +0.3% (0.3 standard deviations above average). See Fig 1-2.

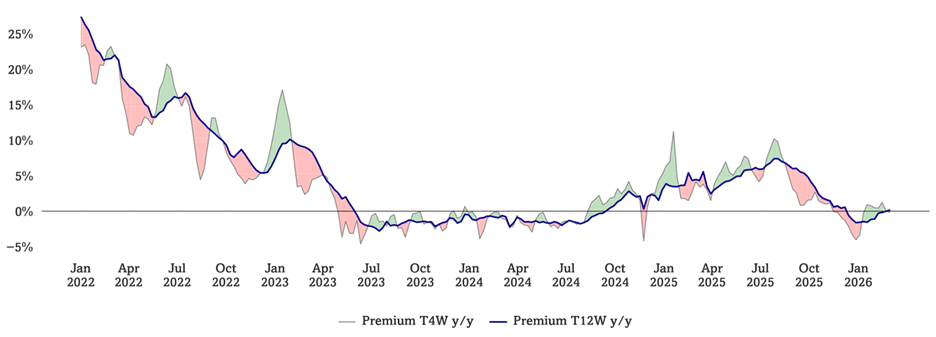

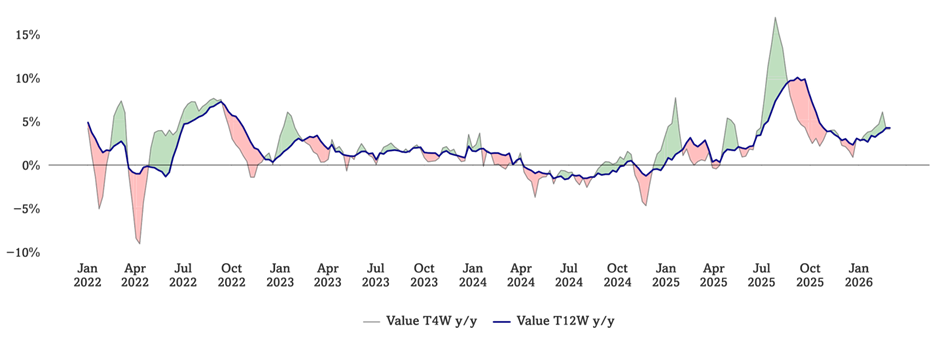

We note moderating spend for our Premium index as Value more resilient. This is particularly interesting in early 2026 with white collar unemployment increasing and our AIR (AI-Resistant) names from Consumer Staples. We use a combination of consumer spending and psychographic monitoring to track “trade up” and “trade down” trends. Optimal’s premium monitor is running up -0.2% y/y on a T4W basis and +0.2 y/y on a T12W basis, running 430 bp (1.0 standard deviations below average) and 410 bp (1.1 standard deviations below average) respectively below our Value Monitor, which is running up +4.1% y/y on a T4W basis and up +4.3% y/y on a T12W basis. See Fig 3-6.

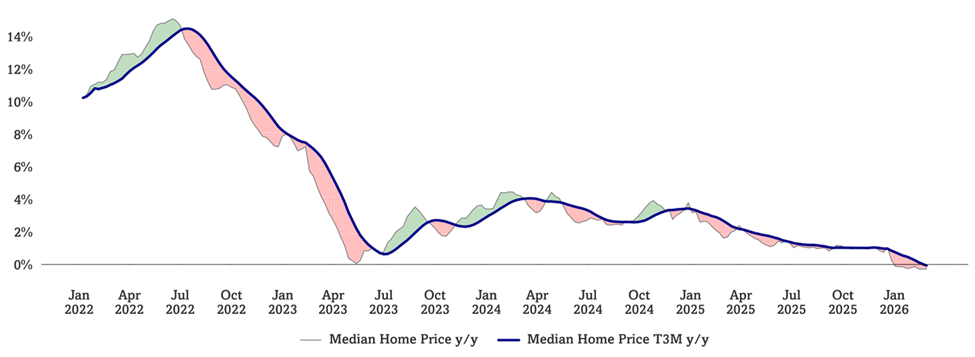

Consumer housing “kinetic energy” continues to show better early signs for more robust 2H26 activity. Refinance applications higher as mortgage rates sit at 6%. US 30Y FRM rate continues to run down, now running down -76 bps y/y on a T4W basis (0.9 standard deviations below average since 2020). MBA’s mortgage applications for purchase continue to run up +8% y/y while refinance applications running up +132% (a low base, but a necessary step to create eventual velocity). Median home prices are flat y/y (-1.3 standard deviations below average since 2020). Roughly 18% of Americans sell, build, fix, lend to, and furnish homes – velocity matters for the economy. See Fig 7-10.

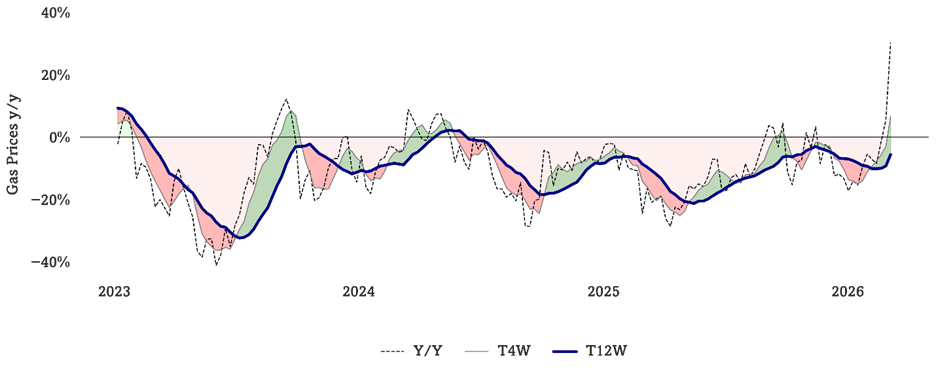

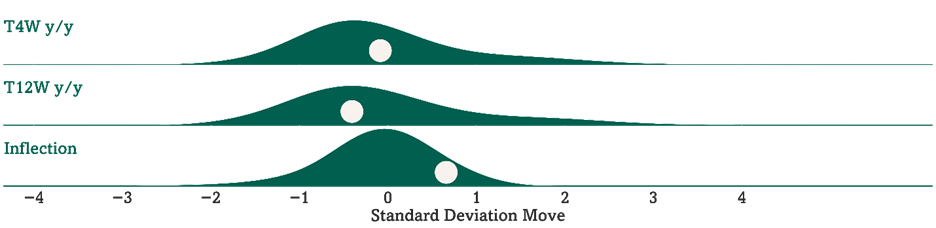

Gasoline prices have accelerated upwards in response to the war in Iran, up +30.3% y/y for the week ending last Friday and up +6.1% already today relative to last Friday. Gas prices ran up +6.6% y/y on a T4W basis and down -5.7% y/y on a T12W basis, corresponding to +12.3% inflection between shorter- and longer-term trends (0.7 standard deviations above average since 2017, which includes 2021 spikes, and 1.9 standard deviations above average since 2023). It is worth noting, US discretionary consumer comp store sales broadly decelerated when y/y prices were +30% in the fall of 2007. We have had lots of recent conversations on oil and fuel prices due to developments in Iran and Venezuela, and prices have increased dramatically this week as investors become wary of a possibly extended conflict in Iran. Generally, lower-income consumers spend about 5% of their total spend on fuel, and higher-income consumers spend about 2.5% – so a 10% move in gas prices drives 25-50 bp headwind or tailwind. Utilities (electricity and heating fuel) run from about 9% of lower-income household spending to 4% for higher-income households. Duration of change matters – eventually causing Consumer Sentiment shifts, which then drive more or less discretionary spending. On the cost side, Feeney noted last week that the Optimal Cost Factor continues to work lower, down -12.5% y/y. Higher energy & oil prices implications will continue to develop in the coming weeks. See Fig 11-12.

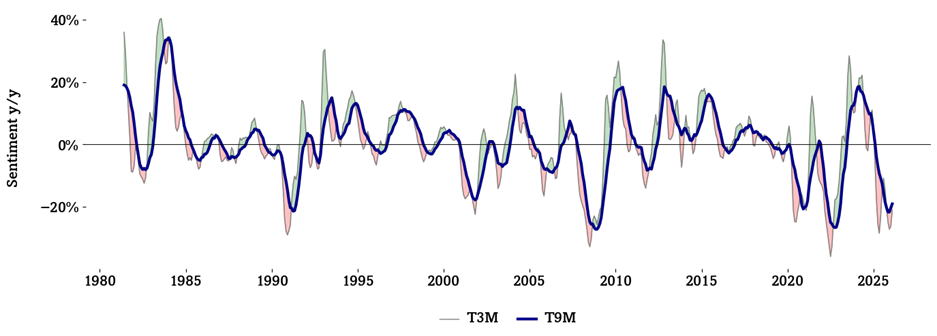

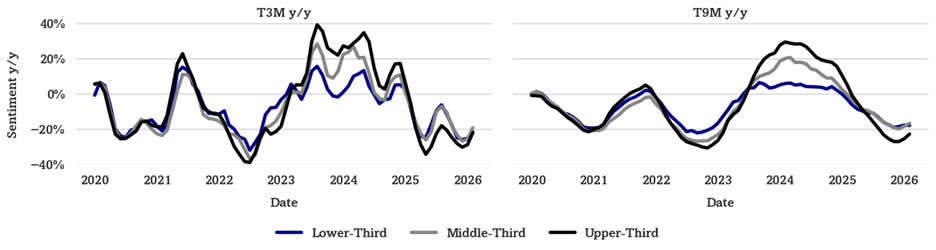

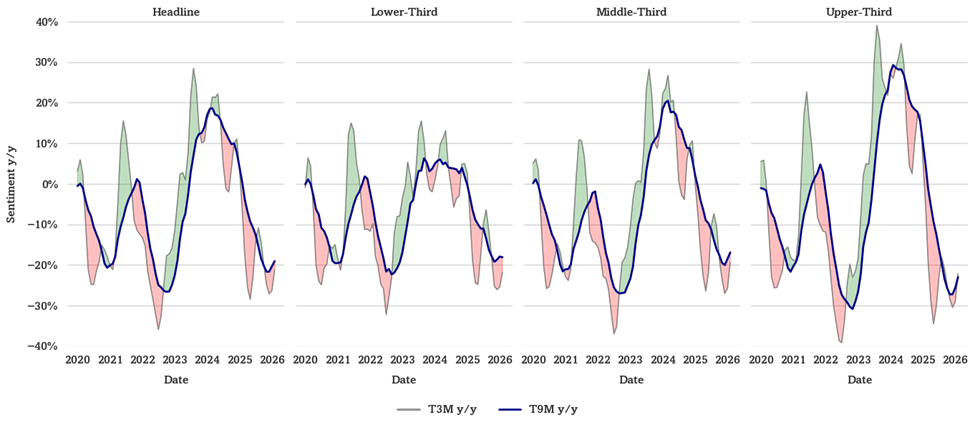

Rate of change is less bad for Consumer Sentiment as it is now down -21% y/y over the past three months, but is only down -13% y/y in February for all respondents -9% for higher-income respondents. Overall, headline Sentiment has declined -21% y/y on a T3M basis (1.7 standard deviations below average) and -19% y/y on a T9M basis (1.8 standard deviations below average). This compares to -20% y/y on a T9M basis last month, marking the third month since late 2024 and fourth month since early 2024 where longer-term Sentiment y/y did not decrease from the prior month. Upper-third income Sentiment has declined -22% y/y on a T3M basis (1.6 standard deviations below average), after declining -29% y/y T3M last month. Middle-income Sentiment has declined -19% y/y on a T3M basis (1.5 standard deviations below average) compared to -26% last month, and lower-income Sentiment has declined -22% y/y on a T3M basis (1.9 standard deviations below average) compared to -25% last month. See Fig 13-16.

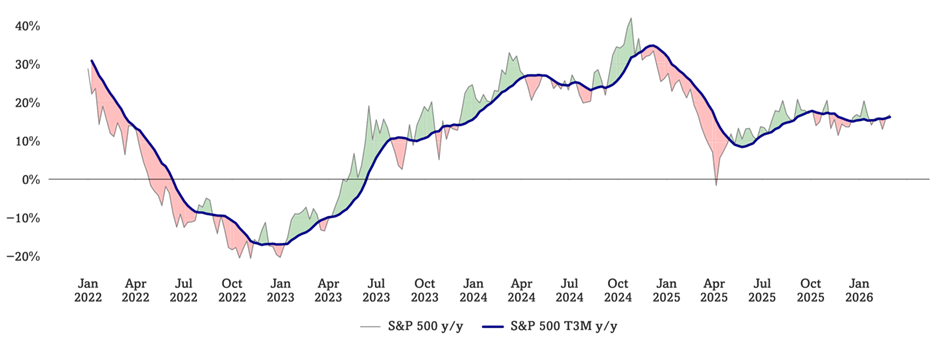

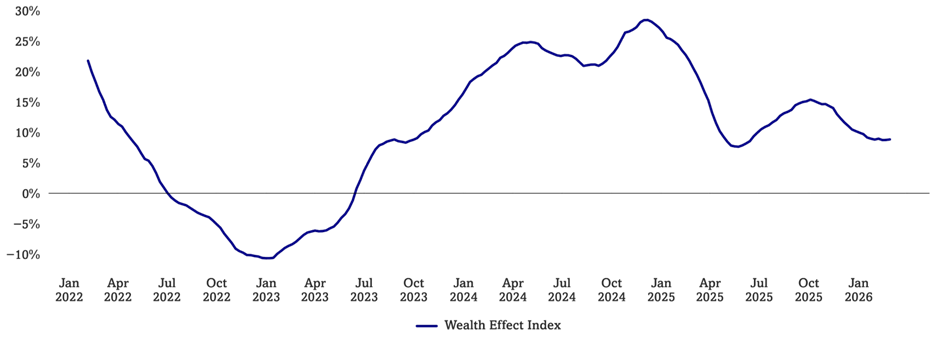

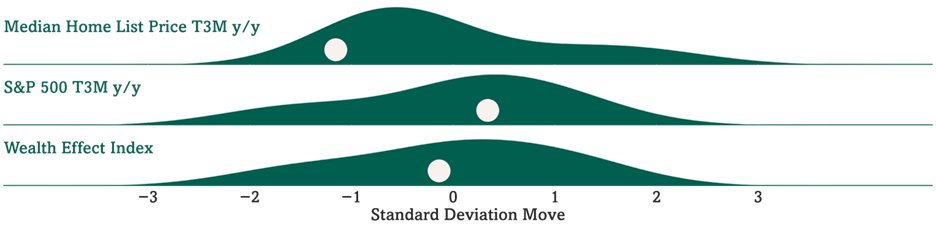

Consumer Wealth Effect Index still below historical average. Optimal Advisory’s Wealth Effect Index is at 8.8% y/y (0.1 standard deviations below average since the start of 2022). This metric was running +15.4% y/y in October 2025. With home prices flat y/y and equity returns moving lower in recent days we note the “flywheel” of wealth effect is more muted. See Fig 17-20.

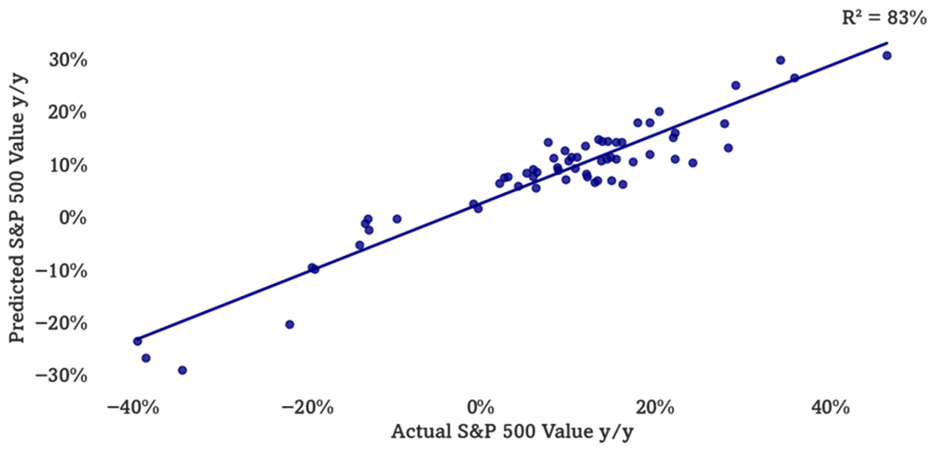

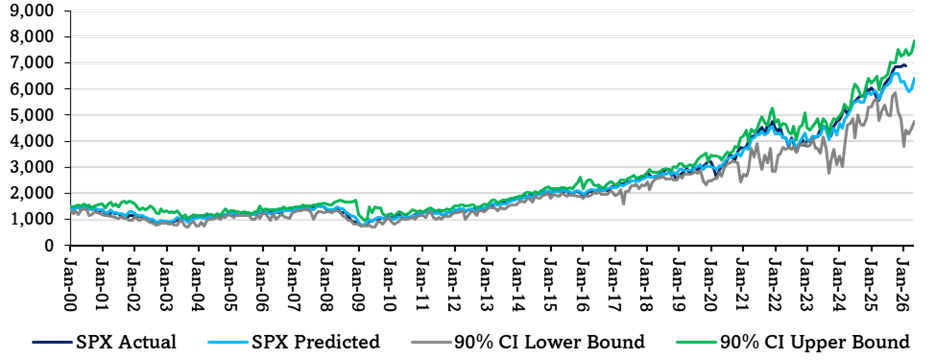

Multifactor Macro Market Model suggestive of softness, rebound. Optimal’s Multifactor Macro Market Model projects the S&P 500 as well as bull and bear cases based on lagged data for 12 macroeconomic factors. The model suggests the S&P 500 to fall to just below 6000 by next March, before rebounding back up to 6400 by May. We use this model as a guide to how macro would guide the market, given our analysis of current variables. This is, of course, outside of other factors at work. See Fig 21-22.

Additional Upcoming Optimal Virtual Meetings

Globally Distributed AI Infrastructure and what it means for Agentic Commerce, AI Devices, and Experiences

March 13th @ 11AM ET

Hosted by: David Schick – Managing Partner & Co-Founder

Sports & Sports Betting Ecosystems with Danny Funt

March 20th @ 11AM ET

Hosted by: David Schick, Jonathan Feeney, & David Katzman – Vice President

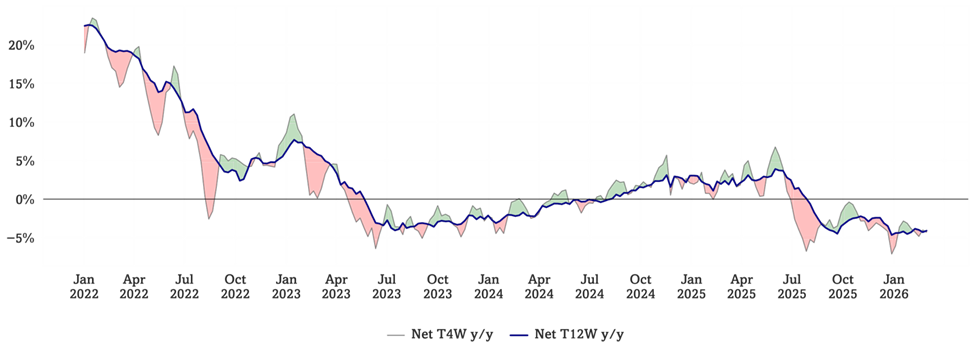

Figures 1-2: Optimal Advisory Consumer Velocity Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Consumer Spending y/y Relative to Historical Average

Source: Optimal Advisory Analysis, Bloomberg Second Measure

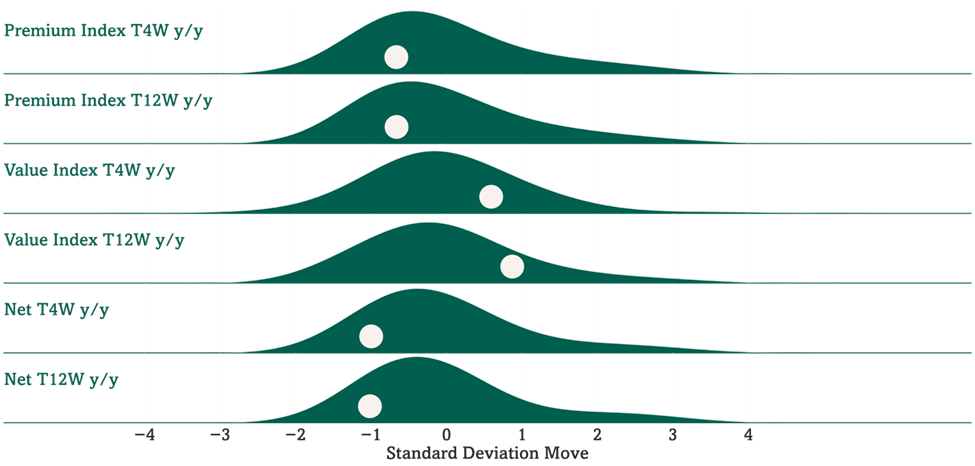

Figures 3-6: Optimal Advisory Premium vs Value Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure, Google Trends

Optimal Advisory Premium vs Value Indices Relative to Historical Averages

Source: Optimal Advisory Analysis, Bloomberg Second Measure, Google Trends

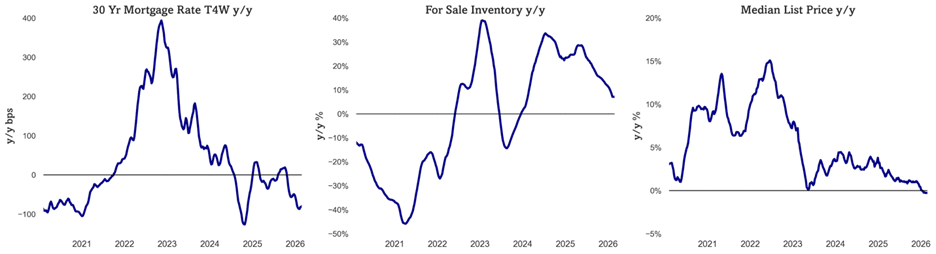

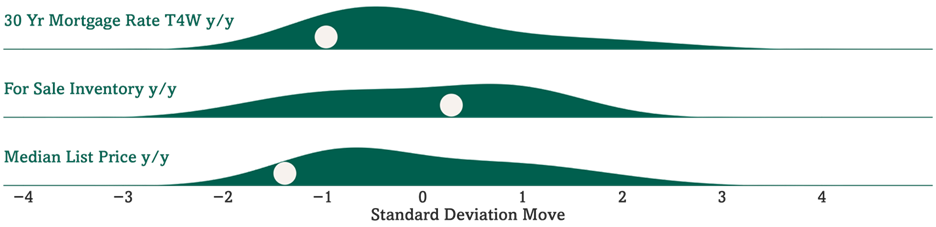

Figures 7-10: Housing Kinetic Energy

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Mortgage Rates, For Sale Inventory, & Median List Price y/y Relative to Historical Averages (Since 2020)

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Figures 11-12: Gas Prices y/y

Source: Optimal Advisory Analysis, Bloomberg

Gas Prices y/y Relative to Historical Averages (Since 1992)

Source: Optimal Advisory Analysis, Bloomberg

Figures 13-16: Consumer Sentiment T3M and T9M y/y

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Sentiment y/y by Income Tercile Relative to Historical Averages

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Comparison of Sentiment y/y Across Income Terciles

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Figures 17-20: Consumer Wealth Effect & Components y/y

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Median Home Price y/y, S&P 500 y/y, & Wealth Effect Index (Since 2022)

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Figures 21-22: Optimal Advisory Multifactor Macro Market Model

Historical Test Predictions vs. Actual (On Test Data Only)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 (Including Training & Test Data) with Confidence Intervals

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

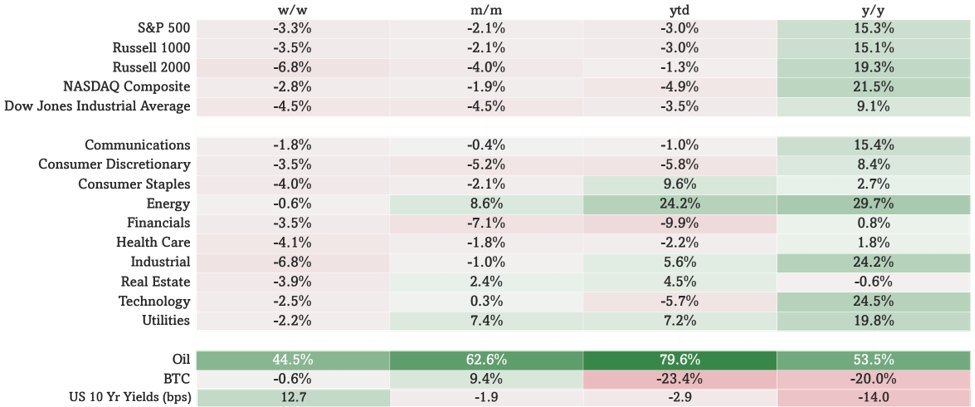

Figure 23: Index & Sector Performance

Source: Optimal Advisory Analysis, Bloomberg, prices at intraday 3/9/2026