Rare Spending Streak; This Week in Store Pics – DKS HD LOW WMT LIDL; Spend Muted but More Stable: Macro Monday

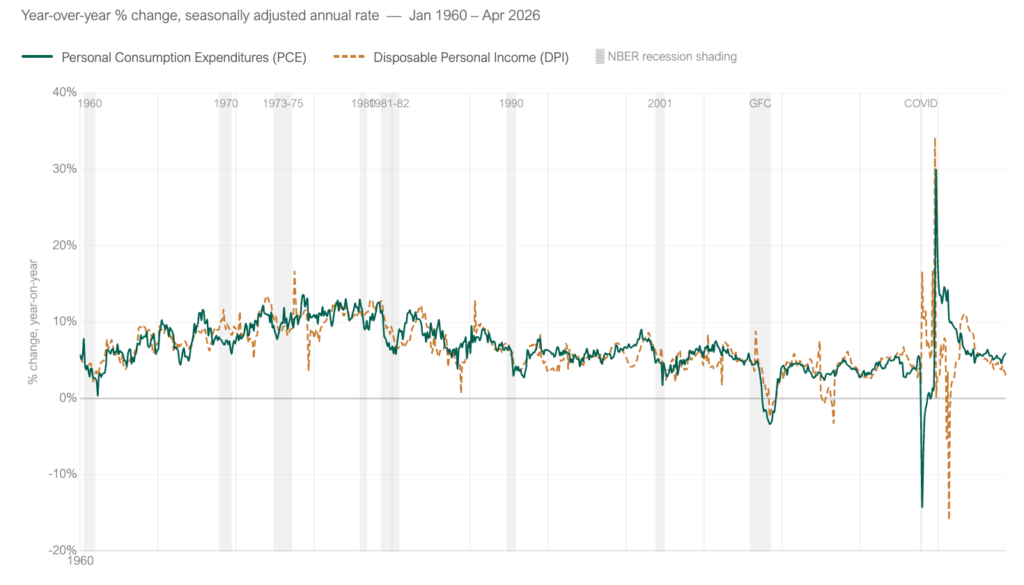

Summary: (1) We call out an economic momentum risk factor … see Chart of the Week … spending has outpaced income for 22 months in a row, this is unsustainable and only the second time a streak this long occurred in the last 50 years (and the other streaks generally preceded slowdowns); (2) This Week in Store Pics we note athletic footwear intros and promos at DKS … HD and LOW seasonal items into summer … WMT LIDL with doors 100 feet apart, pics at end of note; (3) Consumer Velocity ticked up slight to +2.4% y/y T4W and the underlying trend still slightly soft vs. post-2022 average, see Fig 1; (4) Housing activity remains largely frozen with 30Y FRM at 6.53% (-39 bps y/y T4W) and home prices flat y/y, though precursor metrics show some positive inflection, see Fig 3-6; (5) Prices have retreated from highs but gas inflation remain the dominant macro signal at +65% y/y T4W, see Fig 7; and (6) Sentiment remains at all-time lows (44.8) for the second straight month, down -14% y/y, with lower-income (-15% T3M) and middle-income (-11% T3M) worsening while upper-income is flat, see Fig 9-12. Optimal’s Jonathan Feeney will unpack The World Cup Catalyst for brand activations on Thursday 6/6 at 11 AM Register for Optimal Virtual Meeting

Chart of the Week: Spending in Excess of Income Streak Reaching Historic Duration

Source: Optimal Advisory Analysis, FRED

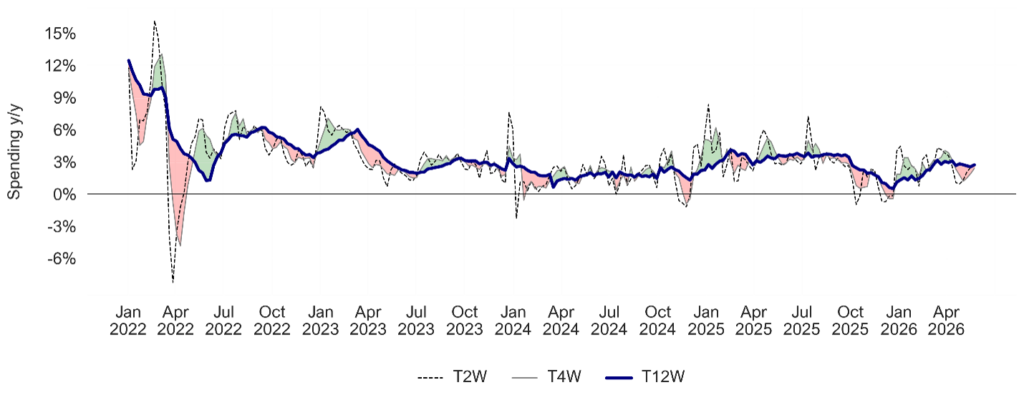

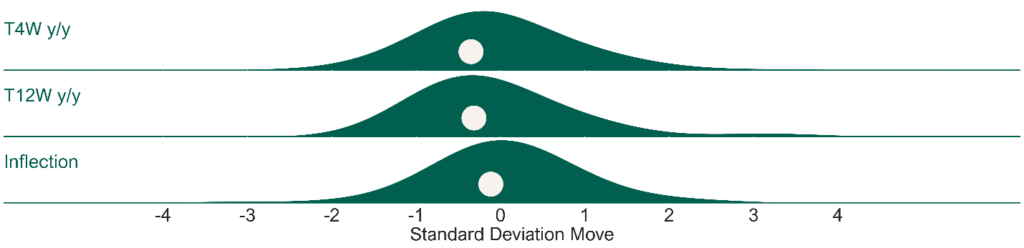

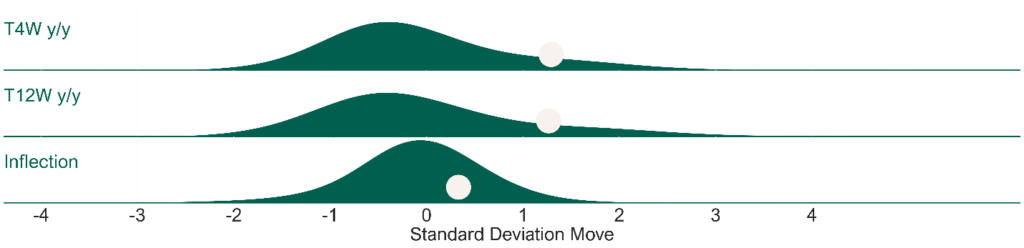

Our Consumer Velocity tracker improved from last week, up +2.4% y/y T4W following +1.9% y/y the prior week, while the T12W trend accelerated slightly to +2.7% y/y (from +2.5%). The underlying trend remains slightly soft (0.4 standard deviations below the post-2022 average on T12W and 0.6 standard deviations below on T4W). The T4W vs. T12W Inflection was -0.3 pts, the sixth consecutive week of shorter-term growth lagging longer-term (although the gap is narrowing). See Fig 1-2.

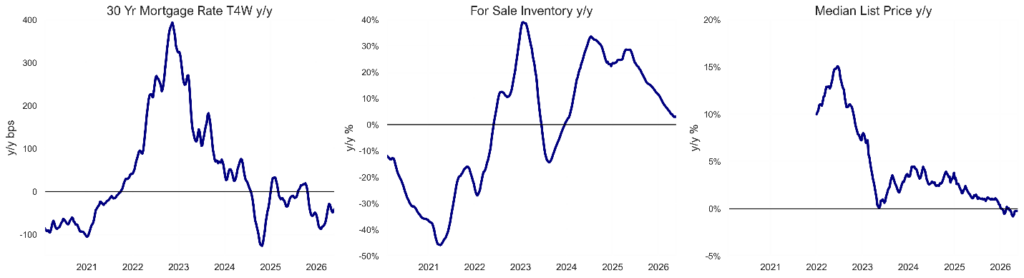

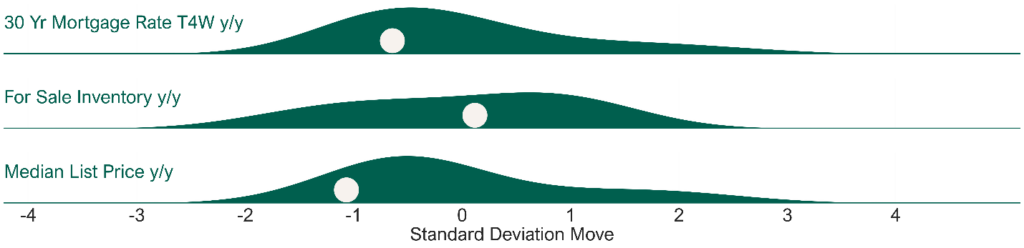

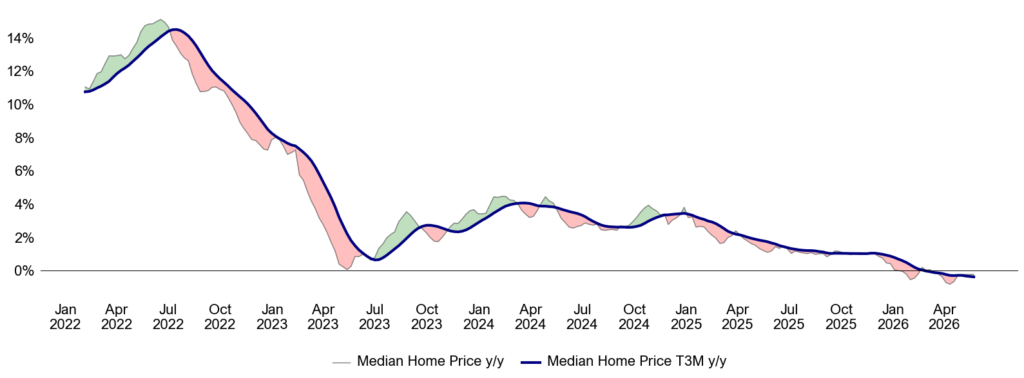

Housing activity remains virtually frozen with precursor metrics also strained by higher borrowing costs. US 30Y FRM rate is up to 6.53%, running down -39 bps y/y on a T4W basis (0.6 standard deviations below average since 2020). MBA’s mortgage applications for purchase index is running up +4% y/y while refinance applications index is running up +20% y/y. Median home prices are flat y/y. Roughly 18% of US GDP is related to the selling, building, fixing, lending to, and furnishing of homes – velocity matters for the economy. See Fig 3-6.

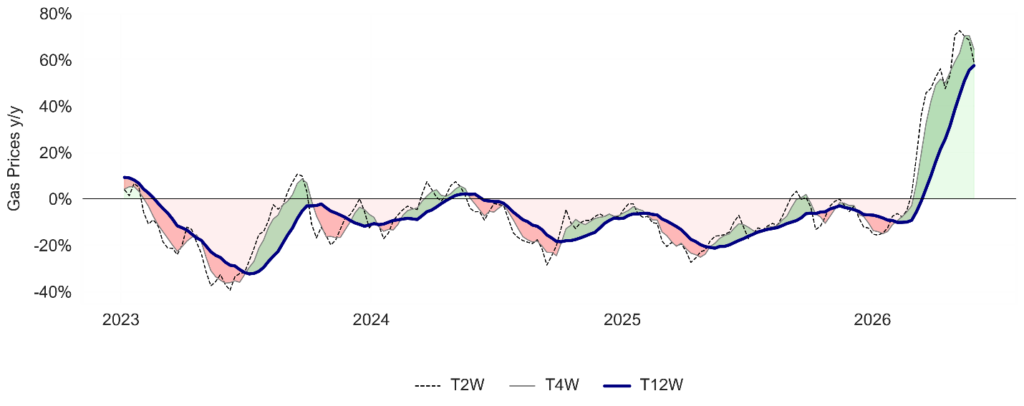

Gasoline inflation remains the dominant macro signal (though gas prices have retreated from recent highs) as the latest weekly print is up +53% y/y, with the T4W now at +65% y/y and the T12W at +57% y/y. The T4W reading is 1.4 standard deviations above average and we are now firmly in the 6-8 week window in which history suggests sustained price pressure begins to materially change consumer spending behavior. We continue to flag that utilities (electricity and heating fuel) run about 9% of lower-income household spending vs. 4% for higher-income households – compounding the squeeze at the bottom of the income distribution. See Fig 7-8.

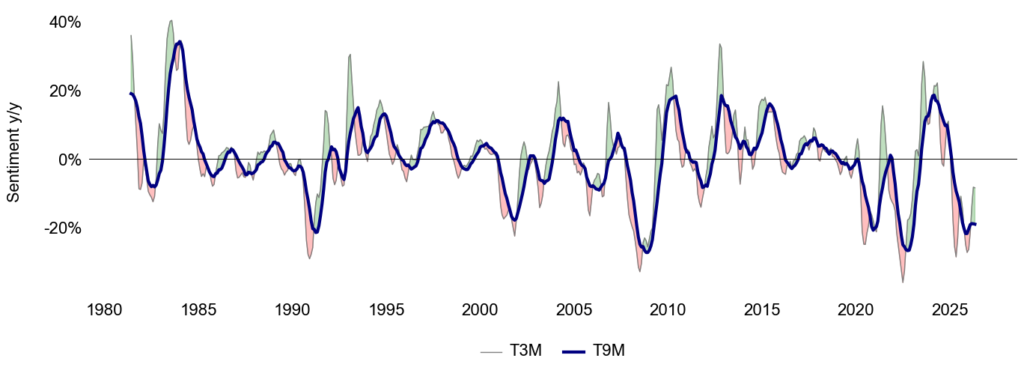

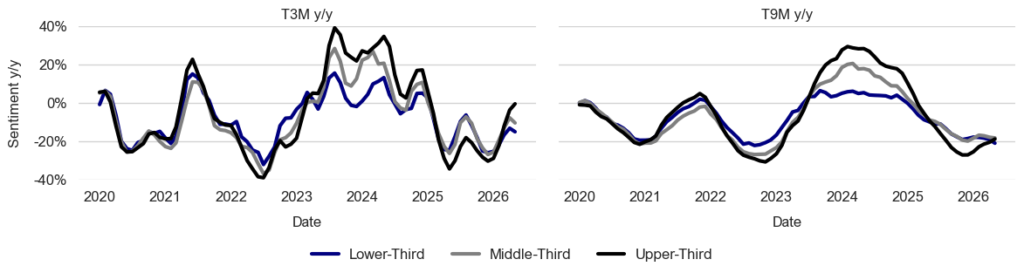

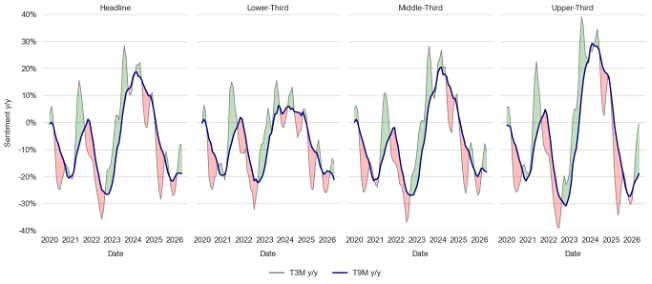

Sentiment is at all-time lows (currently at 44.8) for the second consecutive month, down -14% y/y this month despite lapping exceedingly weak comparisons (revised even further downward). Overall, headline Sentiment is down -14% y/y this month alone and down -8% on a T3M basis (0.7 standard deviations below average) and -19% y/y on a T9M basis (1.8 standard deviations below average). Upper-third income Sentiment is down -1% y/y on a T3M basis (0.1 standard deviations below average), after declining -4% y/y T3M last month. Middle-income Sentiment is down -11% y/y on a T3M basis (0.8 standard deviations below average) after declining -8% y/y T3M last month, and lower-income Sentiment has declined -15% y/y on a T3M basis (1.3 standard deviations below average) compared to -13% last month. See Fig 9-12.

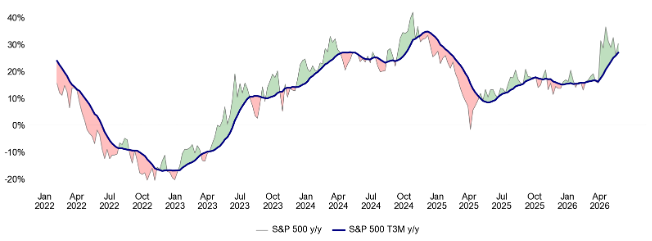

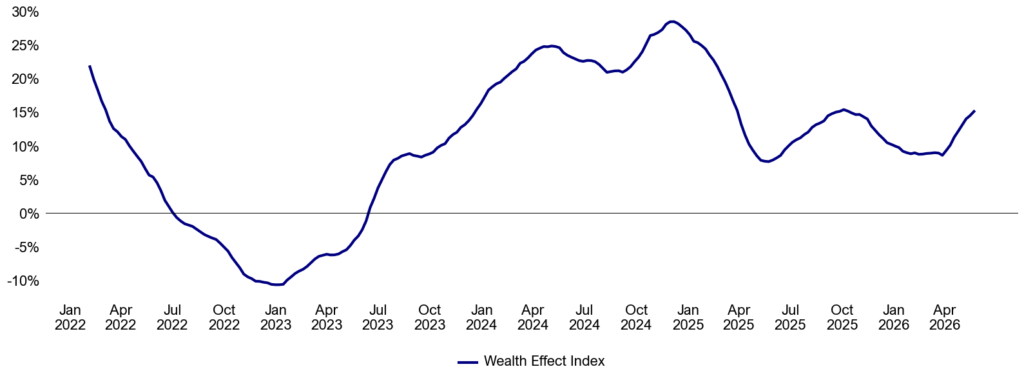

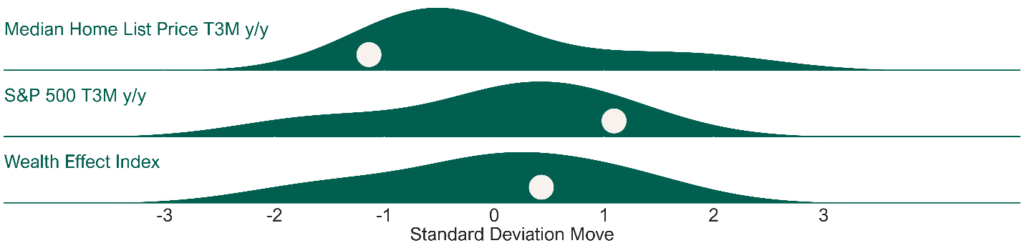

Consumer “Wealth Effect” continued momentum carried by equity returns. Optimal Advisory’s Wealth Effect Index is at +15.6% y/y (0.5 standard deviations above average since the start of 2022 and higher for 9 consecutive weeks). Equity returns have been strong, shrugging off conflict in the Middle East and higher energy prices, while beginning to lap a softer market from Spring 2025. With home prices flat y/y we note the “flywheel” of wealth effect turning higher. See Fig 13-16.

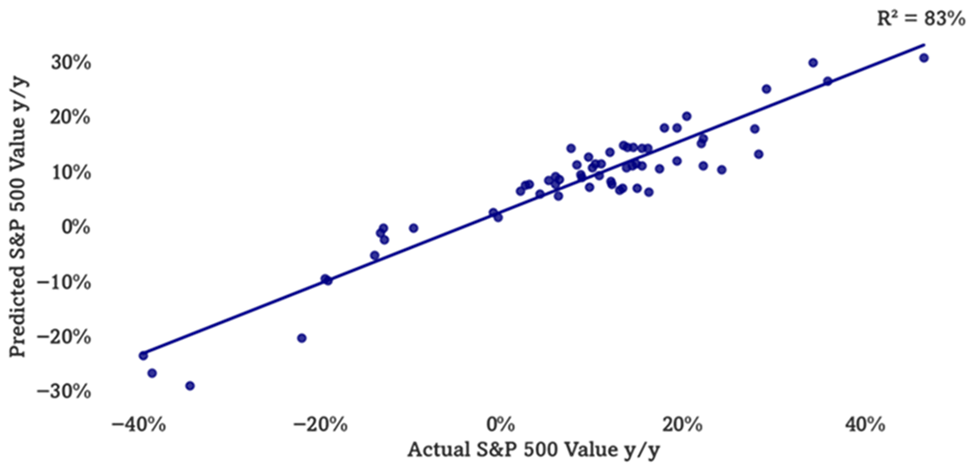

Our Multifactor Macro Market Model has been suggestive of March 2026 softness, rebound. Optimal’s Multifactor Macro Market Model projects the S&P 500 as well as bull and bear cases based on lagged data for 12 macroeconomic factors. The model suggested the S&P 500 to fall to just below 6000 by March, before rebounding back up to 6400 by May. We use this model as a guide to how macro would guide the market, given our analysis of current variables. This is, of course, outside of other factors at work. See Fig 17-18.

Figures 1-2: Optimal Advisory Consumer Velocity Monitor

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Consumer Spending y/y Relative to Historical Average

Source: Optimal Advisory Analysis, Bloomberg Second Measure

Figures 3-6: Housing Kinetic Energy

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Mortgage Rates, For Sale Inventory, & Median List Price y/y Relative to Historical Averages (Since 2020)

Source: Optimal Advisory Analysis, Freddie Mac, Zillow, Redfin

Figures 7-8: Gas Prices y/y

Source: Optimal Advisory Analysis, Bloomberg

Gas Prices y/y Relative to Historical Averages (Since 1992)

Source: Optimal Advisory Analysis, Bloomberg

Figures 9-12: Consumer Sentiment T3M and T9M y/y

Sentiment y/y by Income Tercile Relative to Historical Averages

Comparison of Sentiment y/y Across Income Terciles

Source: Optimal Advisory Analysis, University of Michigan Consumer Survey

Figures 13-16: Consumer Wealth Effect & Components y/y

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Median Home Price y/y, S&P 500 y/y, & Wealth Effect Index (Since 2022)

Source: Optimal Advisory Analysis, Bloomberg, Zillow, Redfin

Figures 17-18: Optimal Advisory Multifactor Macro Market Model

Historical Test Predictions vs. Actual (On Test Data Only)

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

Actual & Projected S&P 500 (Including Training & Test Data) with Confidence Intervals

Source: Optimal Advisory Proprietary Analysis, Bloomberg, FRED, BLS, BEA, OECD, University of Michigan Consumer Sentiment Survey, U.S. Census Bureau, FRB

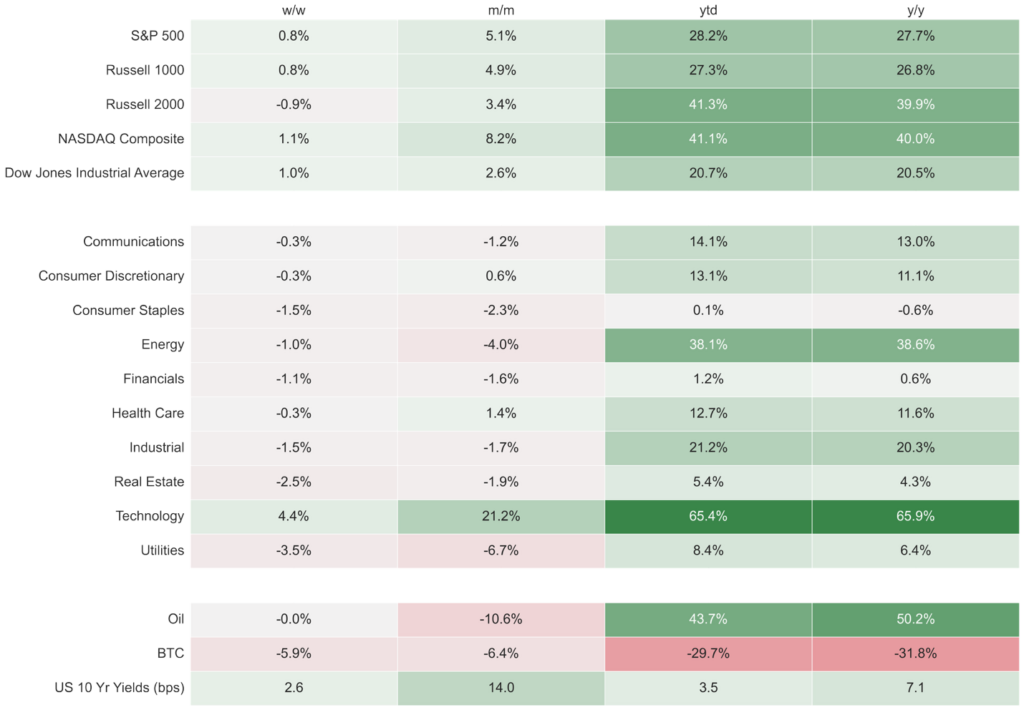

Figure 19: Index & Sector Performance

Source: Optimal Advisory Analysis, Bloomberg, prices at market close 6/1/2026

This Week in Store Pics

Source: Optimal Advisory for all images

DKS Footwear & Apparel, Golf Galaxy US Open Set

HD Seasonal at Entrance

LOW Seasonal at Entrance

WMT – Entrance 100 Feet from LIDL

LIDL – Entrance 100 Feet from WMT